The Year in Review

![]() As the year 2017 draws to a close the economy gives mixed signals of good news and bad news. The past year has not seen any major internal or external shocks that were significant enough to upset development momentum or the economy’s growth trajectory. There were some challenges no doubt. Bangladesh is known to have a severe flood roughly once every decade. This year’s monsoon floods did leave the usual negative footprint with damage to livelihoods and properties that were promptly handled by the nation’s fairly robust coping mechanism for disaster management. But it cannot be tagged as a once-a-decade calamity. The crop sector which bore most of the brunt is on way to recovery from that episode. The other event of note is the influx of some 600,000 Rohingya ethnic minority of Myanmar fleeing pogrom perpetrated on them by the Myanmar military junta. None other than the UN and many more governments have recognized the incident as a case of “ethnic cleansing”, and the international community have been raising their voice to hold the Myanmar government to account for this humanitarian crisis. Bangladeshis have once again shown their kinder gentler side by offering these refugees safety and temporary habitat. They are the responsibility of the UN High Commission for Refugees (UNHCR) which has been actively seeking pledges of aid that is expected to come in drips. Our optimistic assumption is that much of the annual cost of about $600 million will become available and the refugees will be repatriated within a year. A plausible long-tern solution to the Rohingyas of Rakhine State in Myanmar is the Kofi Anan Commission Report that is on the table with wide international endorsement. In the unlikely event that this becomes a longer-lasting festering problem there could be unpalatable economic and social consequences for Bangladesh to endure.

As the year 2017 draws to a close the economy gives mixed signals of good news and bad news. The past year has not seen any major internal or external shocks that were significant enough to upset development momentum or the economy’s growth trajectory. There were some challenges no doubt. Bangladesh is known to have a severe flood roughly once every decade. This year’s monsoon floods did leave the usual negative footprint with damage to livelihoods and properties that were promptly handled by the nation’s fairly robust coping mechanism for disaster management. But it cannot be tagged as a once-a-decade calamity. The crop sector which bore most of the brunt is on way to recovery from that episode. The other event of note is the influx of some 600,000 Rohingya ethnic minority of Myanmar fleeing pogrom perpetrated on them by the Myanmar military junta. None other than the UN and many more governments have recognized the incident as a case of “ethnic cleansing”, and the international community have been raising their voice to hold the Myanmar government to account for this humanitarian crisis. Bangladeshis have once again shown their kinder gentler side by offering these refugees safety and temporary habitat. They are the responsibility of the UN High Commission for Refugees (UNHCR) which has been actively seeking pledges of aid that is expected to come in drips. Our optimistic assumption is that much of the annual cost of about $600 million will become available and the refugees will be repatriated within a year. A plausible long-tern solution to the Rohingyas of Rakhine State in Myanmar is the Kofi Anan Commission Report that is on the table with wide international endorsement. In the unlikely event that this becomes a longer-lasting festering problem there could be unpalatable economic and social consequences for Bangladesh to endure.

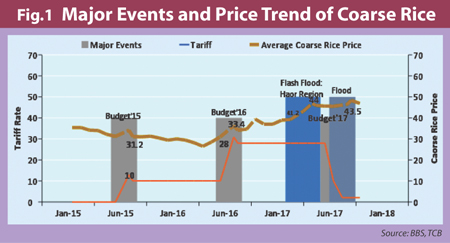

Rice price surge. The economy and policy makers were challenged by a major spike in the price of our staple food grain, rice, in the first half of 2017, adding to the sufferings of flood affected people and the urban poor. Following that episode, price of coarse rice has finally started moderating since October. The country’s food security took the first hit in early April and May when flash floods in the north-eastern Haor regions devastated paddy fields. This was followed by an above average monsoon flooding in August, which washed away around 600,000 hectares of Aman paddy compounding the crippling effect of the flood. These supply shocks coming on the heels of a dubious policy of slapping 10% (FY16) and then 28% (FY17) tariff on rice imports showed up in higher prices of coarse rice in local markets. Coarse rice price shot up to Taka 45.6 per kg in June 2017 from Taka 38.9 per kg at the beginning of the year, and Tk.28 in June 2016 – the combined effect of public stock depletion, floods and dithering tariff policy (Fig.1). It remains an enigma why public stocks were allowed to run down to their lowest levels in years before public procurement through importation (usually a last resort) could be set in motion.

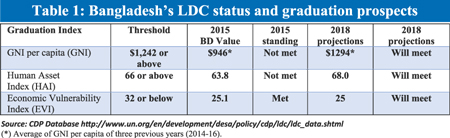

LDC graduation in sight. One good news is that the economy is on track to graduate out of LDC status in the medium term as all the three criteria for graduation will be met in the next triennial review in 2018 (Table 1) with BBS recently confirming Bangladesh’s GNI per capita of $1602 for FY2017.

LDC graduation in sight. One good news is that the economy is on track to graduate out of LDC status in the medium term as all the three criteria for graduation will be met in the next triennial review in 2018 (Table 1) with BBS recently confirming Bangladesh’s GNI per capita of $1602 for FY2017.

In the 2015 triennial review Bangladesh did not meet the GNI and HAI thresholds, but projections for 2018 based on current data indicate that Bangladesh will comfortably meet GNI and EVI thresholds, as well as HAI in the 2018 review, and maintain that position for the 2021 review. A country will normally qualify for graduation from LDC status if it has met graduation thresholds under at least two of the three criteria, in at least two consecutive triennial reviews. Under this rule Bangladesh would qualify for graduation in 2021. However, after CDP recommendation has been endorsed by Economic and Social Council (ECOSOC) and the UN General Assembly in 2024, Bangladesh would benefit from a grace period (normally three years) before graduation effectively takes place (2027). The grace period is designed to enable a graduating country experience a “smooth-transition”, so that the planned loss of LDC status does not disrupt the socioeconomic progress of the country. Bangladesh has the prerogative to opt out of the grace period or even argue to extend it based on adverse developments, should that happen.

In the 2015 triennial review Bangladesh did not meet the GNI and HAI thresholds, but projections for 2018 based on current data indicate that Bangladesh will comfortably meet GNI and EVI thresholds, as well as HAI in the 2018 review, and maintain that position for the 2021 review. A country will normally qualify for graduation from LDC status if it has met graduation thresholds under at least two of the three criteria, in at least two consecutive triennial reviews. Under this rule Bangladesh would qualify for graduation in 2021. However, after CDP recommendation has been endorsed by Economic and Social Council (ECOSOC) and the UN General Assembly in 2024, Bangladesh would benefit from a grace period (normally three years) before graduation effectively takes place (2027). The grace period is designed to enable a graduating country experience a “smooth-transition”, so that the planned loss of LDC status does not disrupt the socioeconomic progress of the country. Bangladesh has the prerogative to opt out of the grace period or even argue to extend it based on adverse developments, should that happen.

As this report goes to press, some 180 ministers of WTO member countries start descending on the placid shores of Buenos Aires, Argentina, where the 11th Ministerial conference is being held. Over the past year, globalization and its compatriot — trade openness — has been much maligned, with some justification stemming from the rising inequalities and joblessness experienced by so many of the developed economies. With the political headwinds affecting globalization, the pros and cons of multilateralism are in focus once again as the wind was taken out of the sails of the emerging mega plurilateral trade and investment partnerships under the onslaught of a dubious Trumpian doctrine of economic nationalism. WTO’s relevance was boosted in the past year thanks to the large number of member countries that ratified two important WTO accords, specifically the Trade Facilitation Agreement (TFA) and an amendment to the WTO’s intellectual property agreement (TRIPS) designed to enhance access to essential medicines among the poorest countries. The latter agreement benefits Bangladesh directly as it extended the LDC waiver for pharmaceutical products to 2033. However, this exemption might not apply to Bangladesh once it graduates out of LDC status, at the latest by 2027.

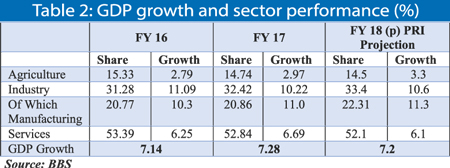

Stable growth performance and outlook. Barring any major man-made or natural calamity in the next six months, the economy appears to be on course to clock another year of 7%+ GDP growth. The latest official statistics on national accounts for FY2017, as reported by BBS (Table 2), basically confirms the estimates presented prior to the presentation of FY2018 Budget, with slight variations to reflect crop damage due to floods and a modest slowdown in manufacturing due to sluggish exports. It appears that the service sector made up for the lost output in agriculture and manufacturing. Apparently, it was higher government current expenditures and public investments that boosted growth and more than offset the deceleration in the growth of exports. The point to note is that expenditure rather than output in government services is what is counted in GDP.

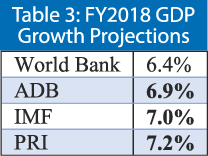

Against this backdrop of domestic economic performance, and based on an assessment of the current state of domestic economic activity and external sector outlook, The Policy Research Institute (PRI) makes the projection of GDP growth of 7.2% for the forthcoming fiscal year (FY2018), marginally lower than the targeted 7.4% growth under the 7th Five Year Plan. This is premised on the modest pick up of agriculture and industry (manufacturing) compared to FY2017 along with some moderation in the service sector. Our development partners have been forecasting

Against this backdrop of domestic economic performance, and based on an assessment of the current state of domestic economic activity and external sector outlook, The Policy Research Institute (PRI) makes the projection of GDP growth of 7.2% for the forthcoming fiscal year (FY2018), marginally lower than the targeted 7.4% growth under the 7th Five Year Plan. This is premised on the modest pick up of agriculture and industry (manufacturing) compared to FY2017 along with some moderation in the service sector. Our development partners have been forecasting  GDP growth rates (Table 3) that regularly hog the headlines, particularly when they diverge significantly from the official estimates. For reasons best known to the World Bank, their projection of GDP growth for FY2018 has been far below those of IMF and ADB, and well below target of the 7th Plan. In the past WB has been effusive about Bangladesh’s growth performance describing it as robust and more stable than growth rate of any developing country. Reasons provided for the low growth projection range from lower LC settlements of machinery imports, construction materials, and other high frequency data that point to low overall growth of the economy. The fact is that these data merely point to but cannot confirm a certain growth rate. It would have been more appropriate for the WB to give a certain range rather than a specific number.

GDP growth rates (Table 3) that regularly hog the headlines, particularly when they diverge significantly from the official estimates. For reasons best known to the World Bank, their projection of GDP growth for FY2018 has been far below those of IMF and ADB, and well below target of the 7th Plan. In the past WB has been effusive about Bangladesh’s growth performance describing it as robust and more stable than growth rate of any developing country. Reasons provided for the low growth projection range from lower LC settlements of machinery imports, construction materials, and other high frequency data that point to low overall growth of the economy. The fact is that these data merely point to but cannot confirm a certain growth rate. It would have been more appropriate for the WB to give a certain range rather than a specific number.

However, at the end of the day, they (i.e. WB, ADB, IMF) all come around and live and work on the basis of official data that comes out of the BBS – the repository of official statistics on national accounts. Under very challenging circumstances and with depleted capacities, the BBS has been engaged in the task of computing national accounts following the methodology designed under the UN system of national accounts (SNA). We are all aware of the weaknesses in this national institution that generates a plethora of national data. Development partners who also rely on this data must use their clout, influence and technical resources, to impress upon the government the critical importance of improving technical capacities in this statistical body rather than engage in public criticism only to undermine credibility of their data that becomes the sole basis for assessing economic performance. It is a fact that none of the development partners have the wherewithal to compute Bangladesh’s GDP which is the compilation of value addition in thousands of economic activities around the country during a given year.

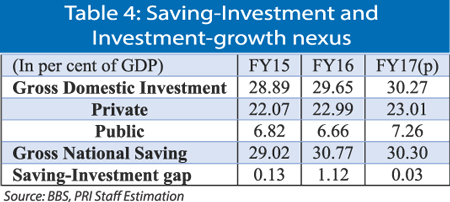

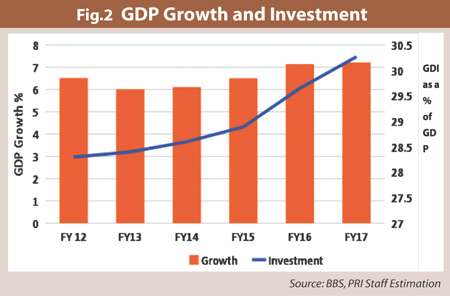

Savings-Investment Scenario. The growth in the level of investment seems to be on the right track in FY17 as it exceeded 30 per cent of GDP at 30.27 per cent in FY2017 (Table 4 and Fig.2). This growth in investment is largely attributed to public investment which was 7.26 per cent as compared to 6.66 per cent in previous fiscal year. Seven mega development projects by the government are well underway and paced up this year. These public projects are expected to have  significant positive impact on future economic activity. The projects are the Padma Bridge, Rooppur Nuclear Power project, Paira Sea Port, the coal fired large power projects of Matarbari and Rampal, Metro Rail and LNG terminal. Furthermore, this progress in physical completion of these projects is expected to boost investor confidence.

significant positive impact on future economic activity. The projects are the Padma Bridge, Rooppur Nuclear Power project, Paira Sea Port, the coal fired large power projects of Matarbari and Rampal, Metro Rail and LNG terminal. Furthermore, this progress in physical completion of these projects is expected to boost investor confidence.

The main policy challenge lies in the efforts to stimulate private investment, which has been pretty stagnant for the past few years and we only experienced a growth of 0.02 per cent this year from previous year. With elections looming in the not-too-distant horizon, anecdotal reports suggest many investors are on a holding pattern thus delaying new investment that should have been. Private investment must get a boost in order to attain the coveted 8% GDP growth at the end of the 7th Plan period.

The main policy challenge lies in the efforts to stimulate private investment, which has been pretty stagnant for the past few years and we only experienced a growth of 0.02 per cent this year from previous year. With elections looming in the not-too-distant horizon, anecdotal reports suggest many investors are on a holding pattern thus delaying new investment that should have been. Private investment must get a boost in order to attain the coveted 8% GDP growth at the end of the 7th Plan period.

National savings, which includes remittance of migrant workers, is essential to achieve higher investment and consequently higher economic growth. The rate of savings and investment to GDP needs to accelerate over time to meet the requirement of 8% GDP growth by 2020. The positive gap between savings and investment is a reflection of under-investment and shows up in current account surplus in the balance of payments in most of the past ten years. The rapid implementation of mega infrastructure projects, public, private and PPP, it is destined to show up in a savings-investment gap and a current account deficit, which is exactly what we see evolving in FY2018.

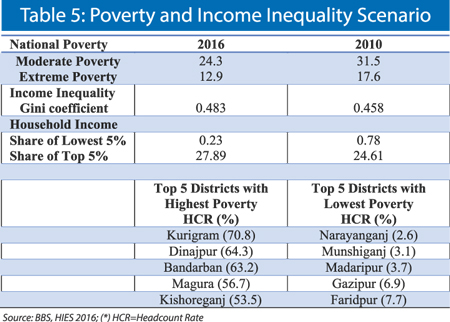

Income inequality rising as poverty declines. The latest status report on poverty is out from BBS, based on the Household Income and Expenditure Survey (HIES) of 2016. The data reveal continued progress in the eradication of poverty (Table 5) as the percentage of population below the upper poverty line (moderate poverty) declined from 31.5% in 2010 to 24.3% in 2016, with extreme poverty declining further to 12.9%. By 2030, if not earlier, extreme poverty appears on track to be eradicated (i.e. zero). The intriguing development is the trend in income inequality.  The Gini coefficient (a standard measure of income inequality across all households) has been trending upwards alongside Bangladesh’s superior growth performance of 6-7% during the past decade. Now, it has risen to 0.483, which is starkly similar to the coefficient in USA, where wealth concentration has resulted in the top 1% of the population owning 40% of the nation’s wealth, almost twice that owned by the bottom 90%. In Bangladesh, we find that the top 5% of households earn 27.9% of total income, which is 121 times the income going to the bottom 5% of households (0.23%), in 2016. In 2010, this was only 32 times (24.61/0.78), showing that the poorest section of the population are getting poorer while income concentration is favoring the richest cohort. Is this a confirmation of the old Kuznet’s Hypothesis that income inequality rises as economic growth accelerates?

The Gini coefficient (a standard measure of income inequality across all households) has been trending upwards alongside Bangladesh’s superior growth performance of 6-7% during the past decade. Now, it has risen to 0.483, which is starkly similar to the coefficient in USA, where wealth concentration has resulted in the top 1% of the population owning 40% of the nation’s wealth, almost twice that owned by the bottom 90%. In Bangladesh, we find that the top 5% of households earn 27.9% of total income, which is 121 times the income going to the bottom 5% of households (0.23%), in 2016. In 2010, this was only 32 times (24.61/0.78), showing that the poorest section of the population are getting poorer while income concentration is favoring the richest cohort. Is this a confirmation of the old Kuznet’s Hypothesis that income inequality rises as economic growth accelerates?

Looking across the country, we find districts like Kurigram still having 70% poverty rate (i.e. 7 out of 10 people are still poor) followed by Dinajpur with 64%. Surprisingly, Narayanganj has the lowest poverty rate of only 2.6%, followed by Munshiganj (3.1%) and Madaripur (3.7%).

Global Economic Outlook. The medium-term growth outlook appears tentative and will depend in part on the new economic relationship within the EU (e.g. how Brexit plays out) and the extent of the barriers to trade, migration, and cross-border financial activity. IMF’s October 2017 report on the global economy and outlook paints a modestly improved picture of the world economy in the current year and next (Table 6). Though global growth is not projected to reach pre-financial crisis levels the good news is that trade growth has finally started to exceed output growth. This phenomenon of trade growth exceeding income growth was the standard feature of the post-war global economy until the financial crisis of 2007-08 broke the trend. It was the signal that trade was the driving force behind post-war prosperity.

That trend — a consequence of rapid globalization – is under siege from political forces in the developed countries who ironically were the champions of free trade and globalization. Rising income inequality and skills mismatch in a period of digital transformation and open trade have led to significant joblessness in those countries giving rise to forces of protectionism and a new wave of economic nationalism. Bangladesh has been one of the biggest beneficiaries of globalization. Its future prosperity with rapid growth and job creation is premised on the idea of an expanding global economy for all goods and services, with robust growth of demand. Therefore, it has a lot of stake in the preservation of the globalizing trends. Enter China’s Xi Ping who is leaving no stone unturned to assume global economic leadership describing globalization as irreversible and arguing the case for a fairer and more balanced globalization. That is a tailwind that the Bangladesh economy richly deserves. Global trade and output growth is an important signal for the prospects of Bangladesh’s exports. According to an UNCTAD report, the slowdown and decline in global trade adversely affected export performance of as many as 112 countries in 2014 and 2015. Bangladesh exports did better than most in 2014-16, though weakening down to 1.7% growth in FY2017. There are signs of modest recovery in Bangladesh exports in FY2018 and the hope is that the recent weakness in global demand will soon be replaced by robust growth.

With 50% of Bangladesh manufacturing production now destined for exports, global economic outlook becomes a highly relevant indicator to watch. The US and German economy, the two largest trading partners of Bangladesh, appear to be in robust shape for the near term. EU growth as a whole though not in robust recovery will be tampered by the pains of Brexit separation. Japan and China appear more stable for the near term which should be good enough for Bangladesh exports. The Indian economy is riding through the two policy shocks arising from the launch of a nationwide General Service Tax (GST) and the demonetization programme. The jury is still out as to what kind of economic boost these two epochal policy initiatives will have on the Indian economy which suffered a bit of a growth setback in recent months.

Ominous signs in the banking sector. The banking sector has been passing through a turbulent period for some time. The sector is still struggling to recover from the recent setbacks caused by large financial scams in a number of state-owned and private commercial banks. The problem seems to be compounded by recent changes in the tenure and family membership of bank boards, some of which have shown signs of ‘group capture’. The proposed amendment to the Bank Companies Act 1991 could lead to further aggravation of the already weak governance in the banking system. The amendment approves increasing the tenure of directors of a private bank from the existing six years to nine years, and allows four members from a single family to be directors in a private bank. This is a reflection of severe weak regulation and governance in the banking sector and means that family ownership (and control) will be predominant in bank management with resulting erosion of corporate governance. Banking supervision, which had improved significantly over the past two decades, is showing signs of decadence. The amendment, cleared by the cabinet, is awaiting parliament approval before becoming law.

The state of state-owned commercial banks (SCBs) is distressing, and there is no relief in sight. Since the government owns the banks, the bank managements have no stake in the efficiency or profitability of operations. Any government is only a transitory owner with little or no real immediate risk. It also has little incentive to manage these banks on a commercial footing because either the losses can be passed on to the citizens through treasury financing based on tax revenues or as continued accumulation of bad loans (i.e. NPL). Instead, there is a strong incentive to use these banks as instruments to finance politically-motivated projects or to distribute political patronage.

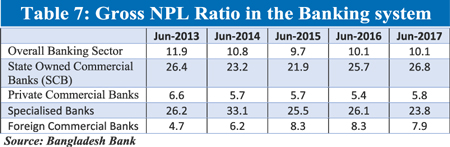

The banking sector is bleeding from bad loans affecting the banks’ profit margin, and adversely impacting business expansion and job creating investments. In a span of 8 years, the amount of non-performing loans (NPLs) in the banking system almost doubled. Where NPL as percentage of total loans and advance in private commercial banks and foreign commercial banks remained  between 5-10 per cent, state owned commercial banks (SCB) held around 27 per cent by end June 2017 (Table 7), for a total of Tk. 320 billion. An internal report on the state of SCBs reveal that the top 20 borrowers held as much as a third of these bad loans. When there is such a concentration of bad loans with big borrowers, recovery becomes nearly impossible, and loan rescheduling or restructuring becomes a fait accompli. Demands on recapitalization year after year out of the public exchequer then becomes inevitable – a clear case of moral hazard. These resources could have been better used to beef up our health and education system.

between 5-10 per cent, state owned commercial banks (SCB) held around 27 per cent by end June 2017 (Table 7), for a total of Tk. 320 billion. An internal report on the state of SCBs reveal that the top 20 borrowers held as much as a third of these bad loans. When there is such a concentration of bad loans with big borrowers, recovery becomes nearly impossible, and loan rescheduling or restructuring becomes a fait accompli. Demands on recapitalization year after year out of the public exchequer then becomes inevitable – a clear case of moral hazard. These resources could have been better used to beef up our health and education system.

Though in better shape than SCBs, private commercial banks (PCBs) are not immune to the NPL hemorrhage. Loan concentration, rescheduling problems, and mismatch of deposit-lending periodicity are festering problems in this group of banks, though in a relatively lesser degree. Flexible measures, including loan rescheduling or restructuring policy favoring powerful people and lack of punishment for fraudulence in banks should set off alarm bells in the banking sector. Needless to say, enforcement of laws is extremely important to control the default scenario in the country today, with total NPL recorded at over Tk.800 billion (about US$8 billion or 20% of national budget) in September 2017.

India, with 70% of bank assets with SCBs, is also in no better shape when it comes to the banking sector. But recently there are signs that it has taken a tough stand in dealing with bad loans effectively. Following orders by the Reserve Bank of India on cleaning up balance sheets, leading corporate houses, including Reliance, Tata, Birla and Essar, were forced to sell their prized assets to repay their bank loans. In order to play the larger role of contributing towards a stable and sound macroeconomic foundations in Bangladesh, there is no option but for the banking sector to go through the path of structural reforms, strong compliance with laws and regulations, and effective governance. Otherwise, the banking sector will remain the Achilles’ Heel of the economy, threatening to implode without warning.

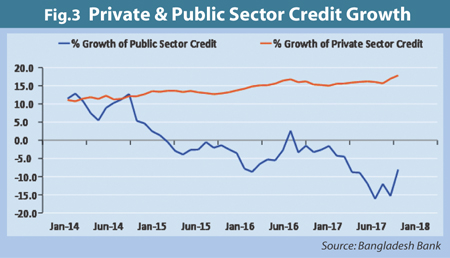

Credit growth promising. Credit from the banking sector is a critical driver of economic growth. Domestic credit in Bangladesh has always been dominated by private sector credit claims. According to Monetary Policy Statement (MPS) 2017, the government is expected to borrow more money from the banking system in the ongoing fiscal year. However, when it comes to actual financing needs of the government, some discrepancies are always observed between the projected and the real growth of public credit, depending on the cash flow situation which is affected by current expenditures and revenue mobilization. The government’s borrowing from the banking system is also influenced by savings mobilization through various savings certificates. As of June 2017, public credit registered a negative growth of 12.02% (Fig.3) compared to BB projection of positive 16.1%. The growth remained negative throughout the year as government was mopping  up too much money through saving instruments. Riding on the high difference in interest rates between bank deposits and NSD certificates, the government has surpassed its annual non-bank borrowing target by a big margin in fiscal year 2017 – but at high interest cost and rising future liability to the exchequer. As banks were flushed with liquidity, the proverbial crowding out of private credit did not occur.

up too much money through saving instruments. Riding on the high difference in interest rates between bank deposits and NSD certificates, the government has surpassed its annual non-bank borrowing target by a big margin in fiscal year 2017 – but at high interest cost and rising future liability to the exchequer. As banks were flushed with liquidity, the proverbial crowding out of private credit did not occur.

In contrast, private sector credit growth hit a 57-month high in July 2017 (up 16.94%) as banks have shifted focus on consumer loans, SME and farm loans to sustain their profitability. However, it was probably the government’s on-going mega infrastructure projects that made major contributions to the higher credit growth in 2017. Some banks have recently started to finance the large infrastructural projects, particularly in the energy sector, which made credit growth vibrant. Private credit also got a boost from import of industrial raw materials and capital machineries destined for large infrastructure and industrial undertakings. Banks are now also focusing on lending to agriculture and small- and medium-sized enterprises to expand their business activities, which is also helping boost private sector credit growth. To stimulate consumption expenditures, the central bank has also doubled the credit card limit to Tk 1.0 million and extended the personal loan ceiling to Tk 0.5 million from Tk 0.3 million. Thus the higher private credit growth in FY2017 is the outcome of several credit boosting initiatives by banks and the private sector.

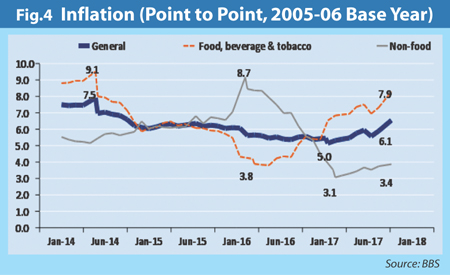

Inflation moderating. At the close of 2011 Bangladesh inflation had reached an all-time high of 11% plus, making it the highest among the South Asian Countries. Thanks to the adoption of an appropriate monetary stance by Bangladesh Bank the inflation rate was brought down to a more desirable level in a span of few years (Table 8). However, after a period of steady decline, an increasing trend of inflation has been witnessed in 2017 due to an uptick in food inflation (Fig.4).  In September, the point-to-point inflation rate hit a two-year-high of 6.12 per cent, primarily due to rise in prices of some food and non-food items. There are signs of moderation in inflation which is down to 6.04 % in October, as reported by BBS.

In September, the point-to-point inflation rate hit a two-year-high of 6.12 per cent, primarily due to rise in prices of some food and non-food items. There are signs of moderation in inflation which is down to 6.04 % in October, as reported by BBS.

In developing countries like Bangladesh where a large amount of household incomes is spent on food, the point to point food inflation is the one to watch closely. Point-to-point food inflation went up 277 basis points to 7.87 per cent in September 2017 from 5.10 per cent in September 2016. This is the highest percentage recorded in over three years. The rise in food inflation reflects mostly rice price increases due to cost push factors such as high tariffs on rice imports as well as production shortfalls due to early floods and blast outbreak and a decline in public stocks. Although tariff has been reduced to 2 per cent in August 2017, a permanent effect of increased rice import on the inflation figure will take a bit of time to have its impact.

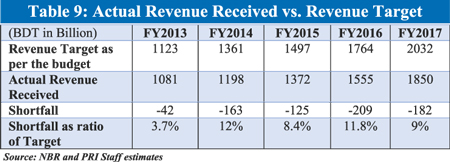

Fiscal Performance challenged. The government has been prone to setting ambitious targets for revenue – tax and non-tax. Though several components of revenue reforms are in implementation phase, the structural deficiencies in revenue mobilization continue to haunt the revenue authority and progress remains slow. Consequently, the actual revenue performance continues to fall short of target year after year, sometimes by a large margin which seems to have been magnifying since 2013 (Table 9).

The huge influx of Rohingya refugees threatens to become a budgetary burden if the problem remains unresolved for too long. According to UNHCR estimates, more than half a million Rohingyas have fled to Bangladesh since the country opened its border on August 25, and the cost of serving each of them is estimated to be around US $1000-1200 in a year. In principle, these stateless refugees are the responsibility of the international community. UNHCR received pledges of more than US $344 million for the Rohingyas in a meeting held in Geneva on 23rd October 2017. Without adequate quantum of international aid to support the Rohingya refugees, the problem could morph into a significant budgetary burden for Bangladesh – something that should awaken all quarters to find a lasting solution to the brewing diplomatic and fiscal challenges.

The huge influx of Rohingya refugees threatens to become a budgetary burden if the problem remains unresolved for too long. According to UNHCR estimates, more than half a million Rohingyas have fled to Bangladesh since the country opened its border on August 25, and the cost of serving each of them is estimated to be around US $1000-1200 in a year. In principle, these stateless refugees are the responsibility of the international community. UNHCR received pledges of more than US $344 million for the Rohingyas in a meeting held in Geneva on 23rd October 2017. Without adequate quantum of international aid to support the Rohingya refugees, the problem could morph into a significant budgetary burden for Bangladesh – something that should awaken all quarters to find a lasting solution to the brewing diplomatic and fiscal challenges.

The much awaited controversy over the uniform VAT law came to a halt when the Finance Minister postponed it for the next two years. However, the lost 2000 billion BDT expected revenue from the new VAT mechanism is expected to slow down revenue growth. Only some of the shortfall could be made up from hikes in rates for basic utilities such as electricity, gas and water supply, with potential inflationary consequences. Notably, the Finance Minister laid down the  largest ever budget in Bangladesh history amounting to 4000 billion BDT, aiming to enhance public investments and the quality of social services, with a big chunk of the revenue expected to be mobilized through VAT. Thus, the aborting of the new VAT sources has raised questions about the viability of the planned expenditures.

largest ever budget in Bangladesh history amounting to 4000 billion BDT, aiming to enhance public investments and the quality of social services, with a big chunk of the revenue expected to be mobilized through VAT. Thus, the aborting of the new VAT sources has raised questions about the viability of the planned expenditures.

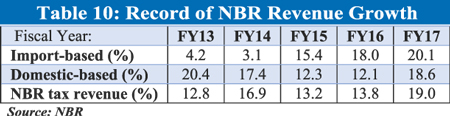

Despite of the shortfall, the trend of revenue mobilization shows that the revenue-GDP ratio (11.2% in FY17) and tax revenue-GDP ratio (9.8% in FY17) is on the mend, although the pace of growth is slow. The growth rate of both domestic and import based revenue is also moving upwards as the three main sources of NBR tax revenue, income tax, VAT and customs duty, have all shown good progress in the recent years (Table 10).

Despite of the shortfall, the trend of revenue mobilization shows that the revenue-GDP ratio (11.2% in FY17) and tax revenue-GDP ratio (9.8% in FY17) is on the mend, although the pace of growth is slow. The growth rate of both domestic and import based revenue is also moving upwards as the three main sources of NBR tax revenue, income tax, VAT and customs duty, have all shown good progress in the recent years (Table 10).

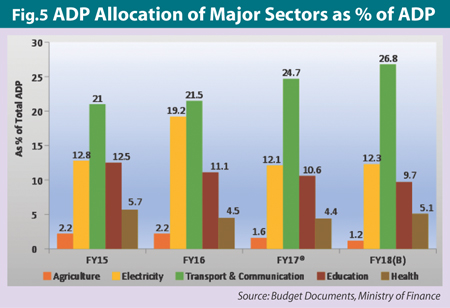

On the expenditure side, the progress of Annual Development Program (ADP) looks comparable to the past few years (Fig.5), showing some sign of government’s diligent endeavor to ensure higher rate of project implementation. The ADP utilization rate (actual ADP as a ratio of budgeted ADP) during FY16 is around 82%, which is 7% higher than the previous year. ADP utilization in July-Oct 2017 shows record growth of 42% over the same period in FY16, with both domestic and aid disbursements up significantly. If this pace continues for the year, we might see record spending and ADP utilization this fiscal. However, the perennial complaint about the quality of expenditure and public services continue to haunt the public institutions.

On the expenditure side, the progress of Annual Development Program (ADP) looks comparable to the past few years (Fig.5), showing some sign of government’s diligent endeavor to ensure higher rate of project implementation. The ADP utilization rate (actual ADP as a ratio of budgeted ADP) during FY16 is around 82%, which is 7% higher than the previous year. ADP utilization in July-Oct 2017 shows record growth of 42% over the same period in FY16, with both domestic and aid disbursements up significantly. If this pace continues for the year, we might see record spending and ADP utilization this fiscal. However, the perennial complaint about the quality of expenditure and public services continue to haunt the public institutions.

The government has enhanced its provision on physical infrastructural investment by around 28% in FY17 (BDT 1271 billion up from BDT 995 billion in FY16). Among the five major sectors, transport and communication is receiving the largest allocation in ADP for the past consecutive years, accounted by Padma bridge and metro-rail projects. Other mega projects to note include Roopur nuclear power plant, Payra deep sea port, Dohazari-Cox’s Bazaar-Gundum rail link, Matarbai coal-fired power plant, etc. The decision to finance the Padma Bridge with our own resources (costing an estimated total of 288 billion BDT) is arguably breaking all records of public expenditure. Dhaka metro-rail project has been moving on full swing with an assessed cost of 220 billion BDT, of which 165 BDT billion is coming from JICA and the rest from the government of Bangladesh. Although the ADP allocation in the power sector has fallen in the current years, nonetheless, the power and energy sector has recorded massive growth with the involvement of private investors, raising the power generation capacity to 15,821 MW until September 2017. Spending on the social sector including education and healthcare facilities have trended modestly downward, which is not a good sign. Implementation challenges usually result in 15% -20% shortfall in ADP utilization than the budgeted amount. That situation is also likely to continue this fiscal year.

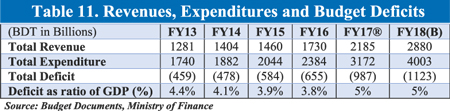

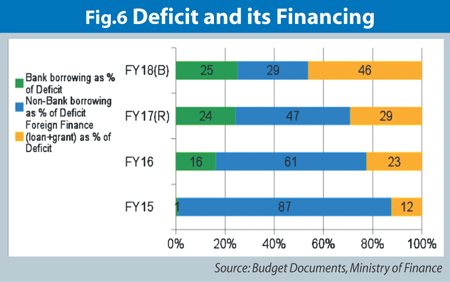

What is notable is that both revenue and public expenditure have more than doubled during the last 5 years (Table 11), though their proportions relative to GDP have not changed much. The budgeted overall deficit to GDP ratio remains at 5% of GDP as in recent years. The positive  development appears to be the rising share of foreign financing of the deficit, which is the least cost option. However, this positive component is offset by the high cost domestic financing component which is non-bank borrowing at above market interest rates. Thankfully, this component which financed 87% of the deficit in FY15, is on the decline and budgeted at only 29% of the FY2018 expected deficit (Fig.6).

development appears to be the rising share of foreign financing of the deficit, which is the least cost option. However, this positive component is offset by the high cost domestic financing component which is non-bank borrowing at above market interest rates. Thankfully, this component which financed 87% of the deficit in FY15, is on the decline and budgeted at only 29% of the FY2018 expected deficit (Fig.6).

Thanks to significantly higher than market interest rates (i.e. rates on bank deposits) offered by National Savings Certificates (NSC), demand for these savings instruments has been strong. High demand of NSC has decreased government’s borrowing from the banking system even further. Reliance on costly non-bank sources of domestic financing shall contribute to swelling of interest burden on future budgets. Foreign financing of the fiscal deficit is the exogenous component of the budget which can be only tentatively prgrammed at budget time. Although the government plans to finance a larger share of its deficit through foreign loans/grants at a lower interest debt during FY18, to what extent this will come to fruition will be seen from donor commitments and disbursements over the next few months.

In sum, the fiscal performance of the economy in FY2018 appears to be challenged from the revenue side primarily due to lack of implementation of the uniform VAT law which widens the deficit in the current fiscal year. Unable to implement the revenue-augmenting law the Government has undertaken a wide range of reforms to streamline revenue collection and expenditure management, in an attempt to fullfill an ambitious budget outlay. If, as in past years, actual public expenditures fall behind targets, the actual fiscal deficit might stay within 5% of GDP, which is within the comfort zone of sustainability.

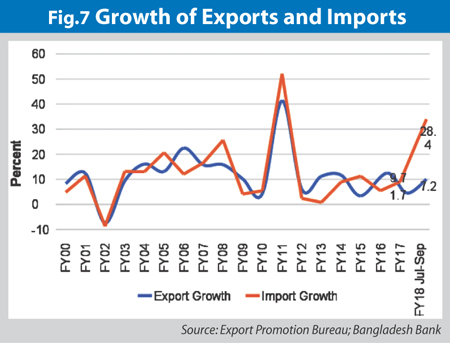

Exports sluggish but picking up. Exports experienced a meagre growth of 1.7% in FY17, the lowest in the last 15 years (Fig.7). A fall of the euro against the US dollar, uncertainty surrounding Brexit and the US elections and a decline in consumption in the West are some of the main factors that contributed to a slowdown in export growth. Bangladesh also received a sharp blow in June this year when the EU, placed Bangladesh on a list of high-risk exporters because of concerns about insufficient safety and security. Air shipments bound for EU nations must now be screened in Singapore, Doha or Dubai. A lot of the airlines are also charging extra due to the re-screening. This has increased costs and delivery times. Bangladesh continues to rely on traditional regions/countries namely the EU and the U.S. for majority of its export revenue. Even though RMG exports are gradually diversifying geographically towards more non-traditional destinations like Japan, Australia and Russia, there is still a long way to go both for RMG and non-RMG exports.

But product diversification of the export basket shows little movement though in FY2016 we exported some 1600 distinct products (at 6-digit HS codes). After readymade garments and footwear, we are yet to find emerging products with staying power, though as many as 1100 products had export values below $1 million, including such unheard of non-RMG items like tricycles, hats and caps, spectacles and objective lenses, cement and various chemical products, and golf equipment. These non-RMG items were exported by some 4000 exporters, most of whom were small exporters also selling in the domestic market where profit margins were typically higher than in exports. Because the trade policy regime has an anti-export bias, these exporters lack the incentive to become large and focusing on exports rather than the domestic market. The net result of this situation is the continuation of export concentration in RMG which accounts for over 80% of our exports.

A modest pick up in exports is observed with growth of 7.43% in the first quarter of FY18 compared to the same period of last fiscal year. The Export Promotion Bureau has set a target of 8.2% export growth for FY18 for which exports would have to amount to approximately $3.2 billion every month for the remaining nine months. It would make sense to also target some progress in export diversification that would aim at reducing export concentration.

Imports on track. Import in FY17 increased by 9.0% (Fig.7) and stood at $43.5 billion from $39 billion in FY16. Almost half of the import payments were spent on intermediate goods which comprise of key raw materials for manufacturing and exports sector. In FY17, sugar, pulses and spices recorded the highest growth in imports of 51.7%, 40.6% and 35.5% respectively whereas fertilizer imports faced the biggest decline of 33%. In FY18, import of rice is expected to increase as a consequence of the floods of 2017. According to the Ministry of Food, Bangladesh imported more than 1.0 million tonnes of rice in the July-October period of FY18. In August, the government cut a duty on rice imports for the second time in two months. The lower import duty has prompted purchases by private dealers. Bangladesh has approved the purchase of rice from India, Myanmar and Thailand. It has already secured deals with Vietnam and Cambodia as it looks to import a total of 1.5 million tonnes of rice in the year to June 2018.

As the global economy shows signs of strengthening and trade flows are gathering momentum, Bangladesh can look forward to see a rebound in its exports. But this trade recovery still remains fragile, and cannot be taken for granted. Related to this an over-valued taka remains a concern not only for exports but also for remittances. Furthermore, total reliance on unskilled labor-intensive exports can prove to be self-defeating in the long run when the reliance on unskilled labour in the context of rapidly changing technological innovations and increased industrial automation (a la 4th Industrial Revolution) can prove to be an unviable option for export-oriented industrialization of the future. While opportunities are still there for Bangladesh to continue to focus on labor-intensive products like RMG and footwear in the near to medium-term, how long that competitive advantage will last is difficult to predict. That creates the necessity for Bangladesh to position itself to take advantage of new opportunities resulting from technological changes and innovations. That means more resources should be directed towards skill development as well as reskilling of the labor force where necessary to enable the country to take advantage of newly emerging opportunities. Bangladesh is behind our comparators in skill development, spending only

As the global economy shows signs of strengthening and trade flows are gathering momentum, Bangladesh can look forward to see a rebound in its exports. But this trade recovery still remains fragile, and cannot be taken for granted. Related to this an over-valued taka remains a concern not only for exports but also for remittances. Furthermore, total reliance on unskilled labor-intensive exports can prove to be self-defeating in the long run when the reliance on unskilled labour in the context of rapidly changing technological innovations and increased industrial automation (a la 4th Industrial Revolution) can prove to be an unviable option for export-oriented industrialization of the future. While opportunities are still there for Bangladesh to continue to focus on labor-intensive products like RMG and footwear in the near to medium-term, how long that competitive advantage will last is difficult to predict. That creates the necessity for Bangladesh to position itself to take advantage of new opportunities resulting from technological changes and innovations. That means more resources should be directed towards skill development as well as reskilling of the labor force where necessary to enable the country to take advantage of newly emerging opportunities. Bangladesh is behind our comparators in skill development, spending only  2.3 per cent of GDP on education compared to the international average of 3.5 per cent. Therefore, to face the challenges of the future, Bangladesh not only needs to focus on today’s jobs but also on developing skills for tomorrow’s jobs.

2.3 per cent of GDP on education compared to the international average of 3.5 per cent. Therefore, to face the challenges of the future, Bangladesh not only needs to focus on today’s jobs but also on developing skills for tomorrow’s jobs.

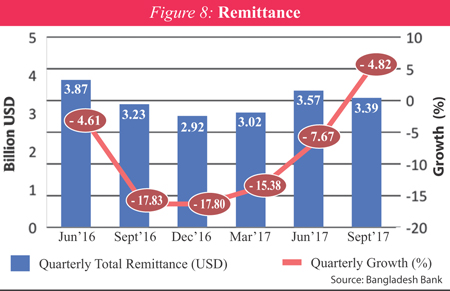

Remittance woes continue. Remittance has been on a decline since last fiscal year, registering a decline of -14% in FY17 but is heading towards a positive trend in FY18 (Fig.8-9). The slump in  FY17 was due to lingering weaknesses in the Gulf Cooperation Council economies- consisting of some of the top destination countries for Bangladeshi migrant workers- as a result of the low oil prices and burgeoning fiscal deficits. The oil exporting countries in the Gulf region struggled with low oil prices and their commitment to cutting crude output per last year’s November OPEC deal which ultimately had repercussions on investment and household consumption. Some other factors which contributed to the slump include the rise in a negative sentiment against immigrant workers in the US and the UK owing to U.S. elections and Brexit, cautiousness in international money transfer operations and the large discrepancy between formal and informal exchange rates. Another reason for the decline in official remittance figures, can be attributed to the gaining importance of informal/illegal channels for transferring funds. Many expatriates are sending money home through the use of mobile financial services (MFS), sometimes referred to as “digital hundi” when not reflected in official inflows.

FY17 was due to lingering weaknesses in the Gulf Cooperation Council economies- consisting of some of the top destination countries for Bangladeshi migrant workers- as a result of the low oil prices and burgeoning fiscal deficits. The oil exporting countries in the Gulf region struggled with low oil prices and their commitment to cutting crude output per last year’s November OPEC deal which ultimately had repercussions on investment and household consumption. Some other factors which contributed to the slump include the rise in a negative sentiment against immigrant workers in the US and the UK owing to U.S. elections and Brexit, cautiousness in international money transfer operations and the large discrepancy between formal and informal exchange rates. Another reason for the decline in official remittance figures, can be attributed to the gaining importance of informal/illegal channels for transferring funds. Many expatriates are sending money home through the use of mobile financial services (MFS), sometimes referred to as “digital hundi” when not reflected in official inflows.

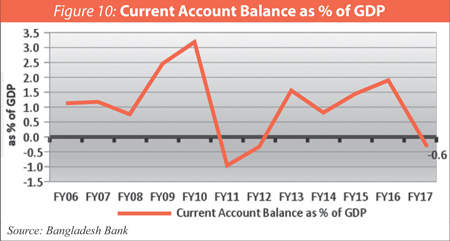

Current Account Balance takes a turn. The unsatisfactory performance in exports and remittance has resulted in a current account deficit of $1.5 billion, and a figure of -0.6% as Current Account Balance as percentage of GDP(Fig.10), where a large deficit has emerged after several years of  surplus, leading to slower reserve accumulation with reduction in the size of overall balance of payment surplus.

surplus, leading to slower reserve accumulation with reduction in the size of overall balance of payment surplus.

Capital and Financial Account. A higher FDI inflow into Bangladesh and comparatively less pressure on the foreign debt repayment facilitated the financial account to stay at a comfortable level. Bangladesh experienced a modest uptick in FDI inflow in 2017 at $2.5 billion, primarily from reinvestment. In FY2017, the highest amount of FDI came from Singapore, with the U.K. and the U.S. taking second and third places respectively. Among the FDI receiving sectors, telecommunication holds the top position, followed by power, gas and textile. There was a large injection of capital by Singapore Telecom (Singtel) to enhance the capital base of Bharati Airtel in the country.

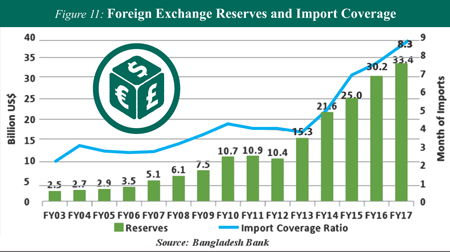

Comfortable Foreign Exchange Reserves. Foreign Exchange Reserves stood at $33 billion as of June 2017 (Fig.11), achieving a growth of 10% compared to last fiscal year. The import coverage of the reserves was 8.3 months which is adequate for a developing country like Bangladesh. However, according to IMF projections, if Bangladesh’s sluggish export growth and decline in remittance inflows continue in FY18, the safe reserve limit should be equal to 9.6 months’ import bill.

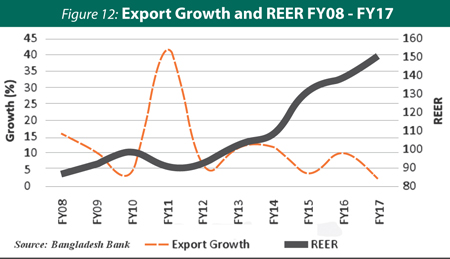

Exchange Rate challenge. There is wide consensus among economists that proper management of the exchange rate is critical for ensuring export competitiveness and a superior export performance. In an economy where export is a key driver of growth, misalignment of the exchange rate could be disastrous for economic growth. In particular, if the exchange rate, nominal or real, appears over-valued, it serves as a major disincentive to exports by stifling profits in an environment where profits are razor thin any way.

Exchange Rate challenge. There is wide consensus among economists that proper management of the exchange rate is critical for ensuring export competitiveness and a superior export performance. In an economy where export is a key driver of growth, misalignment of the exchange rate could be disastrous for economic growth. In particular, if the exchange rate, nominal or real, appears over-valued, it serves as a major disincentive to exports by stifling profits in an environment where profits are razor thin any way.

The real effective exchange rate (REER) estimated by Bangladesh Bank has been trending upward since FY2008 and, except for the export blip in FY11, exports have been sluggish at best (Fig.12). There is no justification for letting the REER appreciate for too long. Fig.12 shows clearly that since the global financial crisis, Bangladesh’s REER has been on the , up 50% by 2017, compared to 2008. Exporters are hurting profusely, to put it mildly, and export performance is arguably sluggish. Getting Tk.79-80 per US dollar of exports for almost five years while global competition has depressed export prices has shaved a good chunk off the already razor thin margins that exporters eke out on the world market. No wonder exporters are searching for relief out of this exchange rate debacle.

The real effective exchange rate (REER) estimated by Bangladesh Bank has been trending upward since FY2008 and, except for the export blip in FY11, exports have been sluggish at best (Fig.12). There is no justification for letting the REER appreciate for too long. Fig.12 shows clearly that since the global financial crisis, Bangladesh’s REER has been on the , up 50% by 2017, compared to 2008. Exporters are hurting profusely, to put it mildly, and export performance is arguably sluggish. Getting Tk.79-80 per US dollar of exports for almost five years while global competition has depressed export prices has shaved a good chunk off the already razor thin margins that exporters eke out on the world market. No wonder exporters are searching for relief out of this exchange rate debacle.

Two other developments related to trade and regional connectivity is worth highlighting.

China’s One Belt One Road’ (OBOR) Initiative. Chinese President Xi Jinping is putting China’s economic prowess behind a Asia-Europe-Africa trade, connectivity and development project to rejuvenate a Silk Road Economic Belt of the 21st-Century, popularly known as the One Belt and One Road (OBOR) initiative. The OBOR idea is to connect Asia, Europe and Africa economically, socially and culturally through sea and land routes. In addition to greater economic integration with China, Bangladesh can also exploit this opportunity to improve its connectivity and transform its economy through trade, investment and greater integration with the OBOR countries. Bangladesh formally joined the Chinese OBOR initiative during President Xi Jinping’s visit to the country in October 2016. Bangladesh is centrally located along the Bangladesh-China-India-Myanmar (BCIM) Economic Corridor and the Chittagong Port is an integral maritime hub that occupies a strategic position along the 21st Century Maritime Silk Road. OBOR can be a major source of investment of billions of dollars in infrastructure for countries like Bangladesh. Cargo transport time is expected to be reduced across OBOR-aligned countries, which will benefit Bangladesh’s trade. China has also pledged to provide various aid and assistance to member OBOR developing countries.

Indian Line of Credit. The third line of credit (LOC) of $4.5 billion to Bangladesh from India for funding infrastructure projects materialized in October this year. The announcement of the line of credit was made during the visit of Bangladesh Prime Minister Sheikh Hasina to India last April. With this India has offered $8 billion loan to Bangladesh in three stages — the highest amount of bilateral loan given by India to any country. This line of credit will also be provided at a concessional interest rate of 1% per annum, with repayment over a period of 20 years including a five-year moratorium. Bangladesh will be using the LOC for funding 17 priority infrastructure projects that include electricity, roads, shipping and ports, most of which will go to enhance cross-border connectivity in the region.

Epilogue. Bangladesh is often cited as a development miracle. Following successful attainment of most of the MDGs, Bangladesh has fully endorsed the agendas outlined in the UN Sustainable Development Goals (SDG) and is actively mobilizing public and private resources to achieve all SDG goals by 2030, most of which appear eminently feasible. For an economy growing at a robust rate, with sustainable debt (internal and external) and fiscal deficits, stable balance of payments and comfortable level of foreign exchange reserves, temporary shocks, natural (e.g. floods), or man-made (e.g. Rohingya influx or burgeoning NPLs) will not upset the cart of economic progress in the near term. But rising income inequality or governance failures in the banking system should raise red flags as they sow the seeds of social discontent and chip away at the roots of an otherwise sound macro economy. These premonitions notwithstanding, the economy and society has shown remarkable resilence in the past and will surely do so in the future. And we all hope to live to see a future that is far brighter than the past.