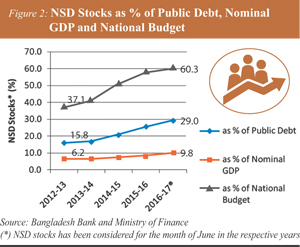

![]() Despite its long history, until recently, Shanchoypatra or savings certificates issued by the National Savings Directorate (NSD) of the Ministry of Finance used to constitute a modest proportion of government budget financing needs. Even in years when domestic borrowing was rapidly growing, non-bank financing through NSD used to be quite modest accounting for a rather small fraction of domestic financing need of the budget. Thus, the outstanding stock of NSD instruments was limited at Tk. 645 billion in end-June 2013, which was 37.1% of government budget, 15.8% of public debt, and 6.2% of GDP. Up until that year the buildup of NSD debt — in relation to the budget size, public debt and nominal GDP — was sustainable.

Despite its long history, until recently, Shanchoypatra or savings certificates issued by the National Savings Directorate (NSD) of the Ministry of Finance used to constitute a modest proportion of government budget financing needs. Even in years when domestic borrowing was rapidly growing, non-bank financing through NSD used to be quite modest accounting for a rather small fraction of domestic financing need of the budget. Thus, the outstanding stock of NSD instruments was limited at Tk. 645 billion in end-June 2013, which was 37.1% of government budget, 15.8% of public debt, and 6.2% of GDP. Up until that year the buildup of NSD debt — in relation to the budget size, public debt and nominal GDP — was sustainable.

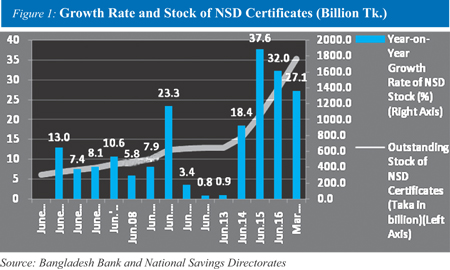

However, the situation changed rapidly since FY14 as the buildup of NSD debt accelerated with the widening of the spread between the NSD interest rates and market interest rates and surged by Tk. 1,280 billion over the next 4 years to Tk. 1,924 billion. If the current policy on NSD interest rate structure is maintained, it is projected that the net sales of NSD instruments will further surge by more than Tk. 700 billion in the current fiscal year (FY18) alone and the outstanding stock of NSD instruments will increase to Tk. 2,624 billion. The projected increase in the current fiscal year is going to exceed the accumulated stock of outstanding NSD debt over the last 70 years until FY13. This is a serious concern and must not be allowed to continue for a long time without giving rise to debt sustainability issues.

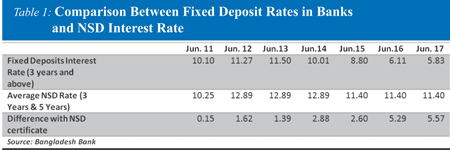

Recent surge in demand for NSD instruments and its consequences: The surge in the stock of NSD instruments started in FY14 and accelerated further in FY16 and FY17, primarily because of the widening of the spread between the average of fixed deposit rates (3-year and above maturity FDR).

As the fixed deposit rates offered by banks continued to decline and declined by almost 3 percentage points to 5.8% in FY17, but the NSD rates remained unchanged, the spread rapidly widened to more than 5 percentage points in FY16 and still remains at such a high level. The household sector responded to such a huge spread by shifting their financial assets to NSD instruments for higher yield, contributing to a massive buildup of NSD debt of the government (Figure 1).

As the fixed deposit rates offered by banks continued to decline and declined by almost 3 percentage points to 5.8% in FY17, but the NSD rates remained unchanged, the spread rapidly widened to more than 5 percentage points in FY16 and still remains at such a high level. The household sector responded to such a huge spread by shifting their financial assets to NSD instruments for higher yield, contributing to a massive buildup of NSD debt of the government (Figure 1).

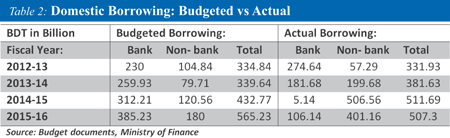

Along with the rapid buildup of NSD debt well beyond the levels envisaged in the budget, there was a corresponding significant reduction of government borrowing from the banking system and in certain years even repayment of government debt to the banking system. This policy essentially entailed that the government was borrowing through the NSD instruments at very high (above market) interest rates, while at the same time paying off treasury bills or cancelling auctions of treasury bills which were available at relatively much lower rates. Because of the “open tap” nature of NSD operations, the ministry of finance (MOF) did not have any control on the volume of borrowing from the NSD system, and accordingly the MOF was forced to reduce government borrowing from the banking system at much cheaper rates.

Along with the rapid buildup of NSD debt well beyond the levels envisaged in the budget, there was a corresponding significant reduction of government borrowing from the banking system and in certain years even repayment of government debt to the banking system. This policy essentially entailed that the government was borrowing through the NSD instruments at very high (above market) interest rates, while at the same time paying off treasury bills or cancelling auctions of treasury bills which were available at relatively much lower rates. Because of the “open tap” nature of NSD operations, the ministry of finance (MOF) did not have any control on the volume of borrowing from the NSD system, and accordingly the MOF was forced to reduce government borrowing from the banking system at much cheaper rates.

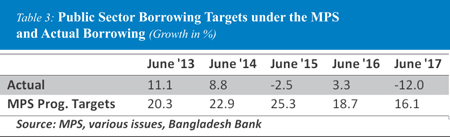

This problem was also reflected in formulating the monetary programme underpinning the bi-annual Monetary Policy Statements (MPS) prepared by Bangladesh Bank. At the beginning of the fiscal year MPS establishes borrowing targets for the government and public sector (including public enterprises) fully in line with the borrowing targets established under the budget. One can easily observe the wide discrepancy between the MPS targets and the actual levels of borrowing, essentially undermining the monetary programme of the Bangladesh Bank.

This problem was also reflected in formulating the monetary programme underpinning the bi-annual Monetary Policy Statements (MPS) prepared by Bangladesh Bank. At the beginning of the fiscal year MPS establishes borrowing targets for the government and public sector (including public enterprises) fully in line with the borrowing targets established under the budget. One can easily observe the wide discrepancy between the MPS targets and the actual levels of borrowing, essentially undermining the monetary programme of the Bangladesh Bank.

This distorted debt management policy has had a number of adverse consequences for a number of areas such as:

* A rapidly growing interest payment burden, which complicates fiscal management in terms of cost and diversion of resources away from important social and economic sectors, which is completely avoidable through proper debt management policy

* Virtual stagnation or even shrinking of the domestic bond market due to very limited issuance of or even withdrawal of treasury bills and bonds from the market, which was already very small and suffering from a lack of appropriate policy support from the MOF and the Bangladesh Bank from market development perspectives

* Adverse impact on the banking system through diversion of its deposit base to NSD, loss of intermediation income due to reduced T-bill and T-bond market activity

* Diversion of potential investment away from the stock market as more and more funds are being invested in the form of NSD instruments

Impacts on fiscal operations and management: The rapid pace of NSD borrowing increased the share of NSD debt from 37% of the total national budget in FY13 to 60% of the national budget in FY17. Such phenomenal growth was never seen in the history of Bangladesh. This is more remarkable given the fact that the size of Bangladesh Budget has been growing at double digit rates in recent years and even with that the outstanding NSD debt reached almost two-thirds of the very large budget. As percentage of national public debt also we observe a similar increase. NSD debt as per cent of total public debt almost doubled to 29% of total debt in only 4 years to FY17. A similar trend is observed in the ratio of NSD debt with respect to GDP, which increased by more than 50% in relation to GDP over the 4-year period to 9.8% of GDP in FY17.

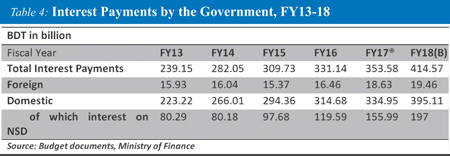

Since NSD debt is the highest cost debt among all domestic and foreign sources, such a rapid accumulation of NSD debt is already having an adverse impact on fiscal management through growing debt service payments. Total interest payments by the government is budgeted to increase by73% in the 5-years period to FY18. Almost the entire increase is attributable to interest payments on domestic debt which increased by 77% during the same period. This increase in the interest payments on domestic debt is primarily attributable to the sharp increase in interest payments on NSD instruments which increased by 246% over the same 5-year period. This trend in interest payments is clearly not sustainable.

Since NSD debt is the highest cost debt among all domestic and foreign sources, such a rapid accumulation of NSD debt is already having an adverse impact on fiscal management through growing debt service payments. Total interest payments by the government is budgeted to increase by73% in the 5-years period to FY18. Almost the entire increase is attributable to interest payments on domestic debt which increased by 77% during the same period. This increase in the interest payments on domestic debt is primarily attributable to the sharp increase in interest payments on NSD instruments which increased by 246% over the same 5-year period. This trend in interest payments is clearly not sustainable.

The subsidy element implicit in NSD debt can be measured in two ways:

The subsidy element implicit in NSD debt can be measured in two ways:

* As the spread or difference between the average interest rate on NDS instruments and the average fixed deposit interest rate (3 years and above). This spread widened from 0.15 percentage point in FY11 to 5.57 percentage points in FY17.

* The spread or difference between the average NSD interest rate and the average interest rate on of T-bill rates (one year). This spread widened from 2.95 percentage points in FY11 to more than 7 percentage points in FY17.

From household perspective the first measure is relevant because this spread measures the actual realised gain that households receive through holding of NSD debt instruments. On the other hand, the second measure is useful from the perspective of public debt management.

On the basis of the first approach, the additional cost to the budget is estimated to have increased from only Tk. 0.95 billion in FY11 to Tk. 106.5 billion in FY17. The estimated fiscal cost under the second approach is even higher at Tk. 134.4 billion in FY17. In both approaches, fiscal costs accelerated from FY14 and reached Tk. 106.5 (US$1.3 billion) to Tk. 134.4 billion (US$1.7 billion) by FY17. To put this cost in perspective, in two years (FY16 and FY17) the government subsidy to NSD holders amounted to Tk. 180-221 billion (US$2.25 -2.76 billion) which is equivalent to 56% to 69% of the estimated cost of Padma Bridge project.

A transfer of this magnitude is indeed a staggering amount and has serious implications for fiscal management and operations from a number of perspectives such as:

* Is this very high level of spending from the budget justified when the government is faced with serious shortfalls in resource mobilisation and has to cut back or limit on many priority programmes including rural roads, social protection, education and health?

* Does this large transfer really serve social protection for the poor and reaches the poor segments of the society?

* Does it foster financial market development or acts against financial market development?

At present, this massive transfer remains outside public and parliamentary scrutiny as this is part of constitutionally mandatory debt service obligations of the government.

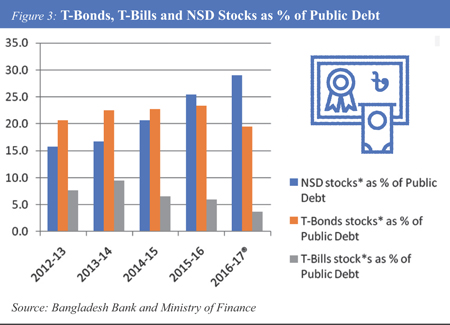

Impact on the domestic bond market: Historically Treasury bond and T-bill markets were expanding steadily, backed by continued government borrowing from the banking system. This contributed to the expansion of the T-bond and T-bill markets until FY15. As the NSD borrowing accelerated since FY14, much of the domestic financing of the budget was being met through that source contributing to an eventual decline in size of the T-bill and bond markets beginning in FY16.

Given the small size of the bond market and the limited range of products, the buyers of the bonds are also specific. On demand side, short-term buyers are only financial institutions and long-term buyers are insurance companies and possibly a few pension/gratuity funds. On the supply side, like most developing countries with underdeveloped bond market, government is the main source of bonds. Currently, the government is primarily refinancing or repaying the maturing bonds and have virtually stopped supplying new bonds. As a result, the secondary market for government securities is losing popularity and importance. Although Bangladesh Bank periodically conducts secondary trading, it is primarily limited to rolling over of existing T-bills and T-bonds and also buying back certain amounts of the securities as per instructions of the government.

Given the small size of the bond market and the limited range of products, the buyers of the bonds are also specific. On demand side, short-term buyers are only financial institutions and long-term buyers are insurance companies and possibly a few pension/gratuity funds. On the supply side, like most developing countries with underdeveloped bond market, government is the main source of bonds. Currently, the government is primarily refinancing or repaying the maturing bonds and have virtually stopped supplying new bonds. As a result, the secondary market for government securities is losing popularity and importance. Although Bangladesh Bank periodically conducts secondary trading, it is primarily limited to rolling over of existing T-bills and T-bonds and also buying back certain amounts of the securities as per instructions of the government.

Over the years the ratio of total stocks of T-bills/ government bonds as a share of total government debt is declining, while the corresponding ratio for the outstanding stock of NSD instruments is increasing. This essentially means that the government’s current policy is promoting accelerated growth of the non-traded NSD bonds, while contributing to a decline in the importance of the tradable financial instruments like bonds. This policy, if continued for several more years, Bangladesh will slowly kill its already modest and nascent bond market over time. Certainly, this would not be in the interest of financial sector development in Bangladesh.

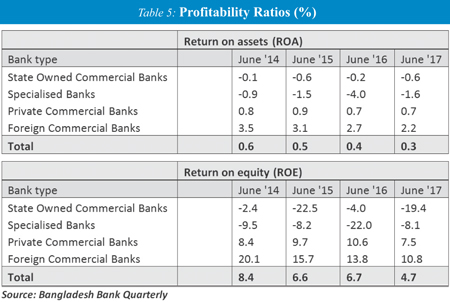

Impact on bank profitability and complications for monetary management: Banking system in Bangladesh is the main pillar of the financial system and the private sector primarily depends on the banking system for its financing needs. Thus, health of the banking system in terms of profitability is critically important for economic development of Bangladesh. Healthy growth in turn depends on the expansion of business activity through lending, including lending to the government.

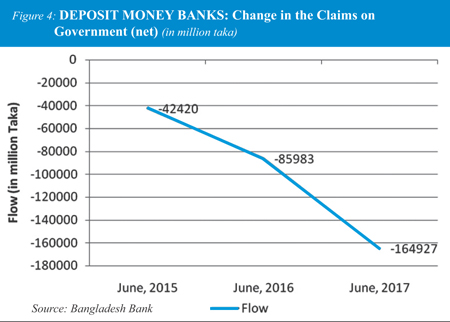

Government sector is an important component of deposit money banks’ overall lending activity. In FY 14, government

borrowing (net) stood at Tk. 1,137 billion which represented about 45.4% of banks’ total lending portfolio. As the outstanding borrowing from the government (net) declined, the share of the government sector in deposit banks’ portfolio rapidly declined to 42.4% of banks total lending portfolio in FY17. As visible clearly from Figure 4, every year since FY15, the government sector has been reducing its exposure to the domestic banking system and the cumulative amount during the three-year period reached almost Tk. 300 billion.

Since the public sector borrowing from the banking system is rapidly declining leading to a huge buildup of excess liquidity, it is also having a deteriorating impact on its profitability. This is clearly manifested in the measures of profitability for the banking system. Return on Assets (ROA) declined from 0.6% in FY14 to only 0.3% in FY17. A similar trend is also observed in terms of the Return on Equity (ROE), which declined from 8.4% in FY14 to 4.7% in FY17. The decline in profitability should not be entirely attributable to the repayment to the banking system by the government, because a number of other factors have also negatively impacted banking system profitability over the same period. Nevertheless, the reduction in government borrowing from the banking system certainly exacerbated the reduction of bank profitability in recent years.

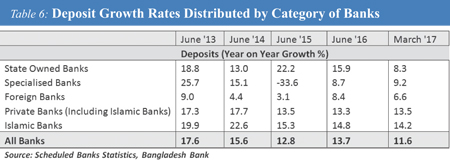

Operations of the banking system are also being seriously impacted by diversion of funds away from the banking system and towards the NSD instruments. This is clearly visible in the marked slowdown in bank deposit growth in recent years (Table 6). The impact of the slowdown in deposit growth was not very strongly felt by the banks because of the prevailing excess liquidity in the banking system until FY16. However, the situation is changing as demand for credit by the private sector is accelerating and already exceeded 17% at the end-August 2017. With credit expansion running at such a high rate and likely to accelerate further, the excess liquidity in the banking system is disappearing fast. In this environment, if the pace of deposit growth continues to remain lacklustre or even decelerates, expansion of private credit will be seriously constrained by the pace of deposit mobilisation undermining expansion of domestic economic activity.

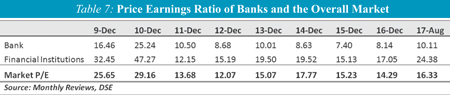

It is particularly noteworthy that the banking system suffered the most in terms of valuation loss, as visible from the persistently low P/E ratio for the banks compared with the overall stock market and other financial institutions in particular. Banks account for about 40% of the market capitalisation, and thus it also dampened the overall stock market performance quite significantly.

It is particularly noteworthy that the banking system suffered the most in terms of valuation loss, as visible from the persistently low P/E ratio for the banks compared with the overall stock market and other financial institutions in particular. Banks account for about 40% of the market capitalisation, and thus it also dampened the overall stock market performance quite significantly.

Recommendations and concluding observations: In addition to fiscal sustainability issues, the continuation of current NSD policy is also seriously undermining the development of the bond market, expansion of the balance sheet and profitability of the domestic banking system, and is also hurting the level of activity in the stock market through potential diversion of funds to the NSD instruments. Bangladesh bond market is already very narrow with limited trading activity. It thus cannot afford any further shock resulting from shrinking or declining government bond issues. Development of the bond market in a systematic manner has long been ignored by Bangladesh policy makers and it is high time that renewed focus is given to the development of this market from both supply and demand sides. Infrastructure development in Bangladesh — be it public sector or PPP-based initiatives — will require long-term financing, which should preferably be secured through issuance of long-tenure bonds and asset based bonds. Like most developing economies, an active bond market can develop in Bangladesh only with initial supplies of public sector bonds. Private sector bond issues will follow the development of the treasury bond market which will also provide the yield curve for private bond issues. No bond or asset-backed securities market can develop in Bangladesh as long as the distortions introduced by the NSD instruments are not removed.

During FY14-16, the banks were largely flushed with excessed liquidity and thus did not feel the pressure from the declining deposit growth in recent years. However, the outlook is changing very rapidly. With the recent acceleration in private sector credit demand (reaching almost 17% as of August 2017) and slower deposit growth, the excess liquidity in the banking system is disappearing rapidly and interest rates are going to increase due to enhanced competition for mobilising savings. A significant cut in the NSD interest rates will contribute to a slower growth in NSD investment and a corresponding diversion of funds to the banking system easing pressure on banks’ profitability and allowing them to expand their asset base faster.

Two types of market-based solutions may be considered. The first and the most clean solution calls for a complete phasing out of the NSD instruments by stopping new sales to customers. NSD instruments were justified as investment instrumentsin the colonial era when banking network was limited. With modern banking system and accessibility of banks to most people, the NSD scheme may well be dismantled for the greater good of the economy. The investment of NSD should be directed to the banking system and the bond and stock markets.

A less dramatic market-based approach may be to link the interest rates on NSD instruments to the corresponding rate of returns on T-bills and T-bonds of similar maturities. From an operational point of view, we may think of certain rules such as adjusting interest rates every quarter. In this approach, the cost of NSD borrowing would be broadly market based and the element of subsidy would disappear. International experience indicates that most countries with national savings programmes have adopted some form of market-based solution and limited access primarily to low income households.

Structural reforms leading to rationalisation of interest rates in line with market rates may also be considered with some rule-based mark up (premium) above the market rate. The mark up over the benchmark market-based rates should be limited to 0.25-0.5 percentage point above the benchmark rates and the benchmark rates should be adjusted every quarter on the basis of the quarterly average rate for the preceding quarter. The proposed markup may only be justified on the ground that it would encourage small savers to go through the inconvenience of buying and getting paid on NSD instruments. The markup should also entail lowering of the current quantitative limits on the amounts of investment in these instruments.

The government needs to act now as the problem is intensifying over time. In less than 15-month time, Bangladesh is going to hold its next general election and it would be imprudent to let this problem become monstrous and stifle the financial sector more severely undermining economic growth and fiscal sustainability. Continuing the status quo until the next general elections to be held in early 2019 also may thus may be imprudent on political-economy considerations. Instead, undertaking NSD reforms on an urgent basis along the lines suggested above will release large amounts of resources which can be used for significantly increasing social sector spending with beneficial impacts on poverty, health and education standards across the country. If properly packaged, reform of the NSD can be made politically attractive as well.