Navigating an economy on edge

Dr. Zaidi Sattar | Sunday, 10 December 2023

![]() Defying a perfect economic storm

Defying a perfect economic storm

From the start, the year 2023 was beset with macroeconomic challenges of the worst kind. The troika of macro indicators – inflation, exchange rate, and foreign exchange reserves – showed signs of volatility that lasted for much of the year and remains unresolved. The long period of macroeconomic stability, both internal and external, that characterized the Bangladesh economy for over twenty-five years seems to have come to an abrupt end in 2023. Challenges have emerged on multiple fronts: spike in domestic prices of essential food products, depletion of foreign exchange reserves, massive exchange rate depreciation, deficits in the financial account of the balance of payments (BOP) resulting in overall BOP deficits, conflicts in fiscal and monetary policy coordination in taming inflation, and so on.

This is nothing short of a perfect economic storm for the Bangladesh economy, unprecedented in scope and intensity of the problems. Add to that the cloud of political bickering interspersed with often violent disruptions to production and overall economic activities via hartal and aborodh. Rough times are ahead as national elections loom and uncertainty becomes the new normal. The economic ramifications of the combined effect of these developments could not be more acute and wide ranging. Such confluence of political and economic challenges in a trade-integrated middle-income economy like Bangladesh breeds capital flight, of which there are many indications.

That said, this is hardly the time to give doomsayers the upper hand. On the positive side, we have the Padma Bridge – the longest river bridge in the country – now in full operation (rail and road links). The first undersea tunnel in South Asia – Bangabandhu Tunnel in Karnafuli – is now open to traffic, a project that was completed in record time. Dhaka Metro Rail now links Uttara with Motijheel slashing travel time to 31 minutes in place of 2-3 hours typical journey on a Dhaka work day. Finally, the country is now fully connected – East, West, North, South – by road network, with full rail connectivity imminent. These megaprojects and more that became operational in 2023 will have game changing impacts with profound efficiency dividends – in terms of time and cost reduction – for the society and economy, quantitative estimates of which will have to be worked out, but suffice it to say that it will be substantial and could add up to 1 per cent to GDP growth over the medium – to long-term.

Our history is replete with disruptions of hartal and aborodh kind – even worse – that were eventually overwhelmed by positive forces that ensured continuation of the steady-state momentum of a growing economy. These are outmoded approaches to political resistance that can no longer be effective means of disrupting the wheels of a dynamic economy. Resilience of the human spirit runs through our economic corridors to sustain the onward trajectory of progress, not decline. History of the past fifty years is testament to that unbound survival spirit of Bangladeshi people.

Global economic outlook and deglobalising trends

The world economy is experiencing a geopolitical firestorm, with two regional wars raging with full fury, while the world economic order gets increasingly fragmented into regional or allied groups. Particularly over the past 30 years Bangladesh economy has become increasingly more integrated with the global commodity and financial markets. Trends in the global economy therefore leave significant imprint on the domestic economy – through domestic prices, export performance, and movements in exchange rate and balance of payments. The latest IMF assessment of the near-term outlook signals “soft landing” rather than a recession in developed economies that matter. Nevertheless, there are strong indications that the international trading system of the past 75 years is under attack. And the immediate casualty is its “efficiency dividend”.

Developments in the global economy over the past year did not leave much to cheer. After an initial period of supply chain disruption following the outbreak of the Russia-Ukraine war, commodity prices moderated somewhat but volatility remains. The evolving geopolitical scenario signals reconfiguration of global alliances with significant impact on the world economic order that prevailed for the past 75 years. Vulnerabilities and uncertainties in the world economy appear ascendant with the sinister rise of economic nationalism, unilateralism, and protectionism in those countries that were the original protagonists of free trade and globalization. The glossary of economic terms is being enriched by newly coined expressions like “homeland economics”, de-risking, re-shoring, friend-shoring, strategic autonomy, and the like. In essence, these are expressions to describe the emerging trend toward greater protectionism as more and more developed economies resort to “industrial policies” with various forms of competing support or subsidies to domestic production. Finally, there is the US-China decoupling scenario gathering momentum by the day which promises to leave a fractured world market under a de-risking scheme of “China+1”. The principal casualty is the efficiency dividend of globalization and its pivotal offshoot – global value chain (GVC) integration. Trade multilateralism is under threat like never before since the creation of the post-War economic order.

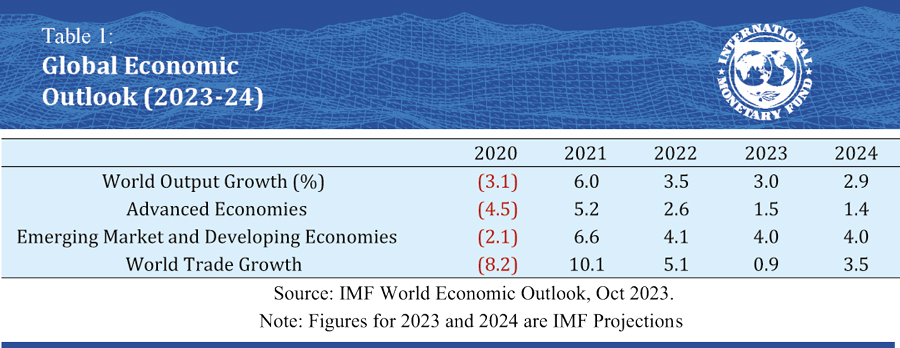

The most eagerly watched indicator of the global economy comes out of IMF’s World Economic Outlook (WEO) that is regularly updated roughly twice every year. Coming out of the recent IMF-World Bank meetings in Washington the latest edition of the WEO gave us a flavor of what is to come in the world economy in the year 2024, after a rather muted assessment of the 2023 world economy. What is clear is that the fast-paced recovery from the Covid-19 pandemic blowout is petering out with prospects of slower growth in the current (3per cent) and next year (2.9per cent). The projections remain below the historical (2000-19) average of 3.8per cent. The slowdown appears to be more pronounced for developed economies than for developing and emerging market economies (Table 1). However, what appears to be most disconcerting is the rate of trade growth which appears to have plummeted to 0.9per cent in 2023 but is expected to pick up above world output growth in 2024. That is a good sign for Bangladesh export prospects.

The most eagerly watched indicator of the global economy comes out of IMF’s World Economic Outlook (WEO) that is regularly updated roughly twice every year. Coming out of the recent IMF-World Bank meetings in Washington the latest edition of the WEO gave us a flavor of what is to come in the world economy in the year 2024, after a rather muted assessment of the 2023 world economy. What is clear is that the fast-paced recovery from the Covid-19 pandemic blowout is petering out with prospects of slower growth in the current (3per cent) and next year (2.9per cent). The projections remain below the historical (2000-19) average of 3.8per cent. The slowdown appears to be more pronounced for developed economies than for developing and emerging market economies (Table 1). However, what appears to be most disconcerting is the rate of trade growth which appears to have plummeted to 0.9per cent in 2023 but is expected to pick up above world output growth in 2024. That is a good sign for Bangladesh export prospects.

Thankfully, IMF assessment suggests that inflation-related policy tightening in major economies is only leading to a “soft landing” without the much talked about impending spectacle of recession in developed economies. Finally, the rise of Asia is noticeable with roughly one-half of global growth now accounted for by Asian economies.

For the Bangladesh economy and its export prospects, global output growth of around 3per cent should not be a matter of much concern as our export performance remained resilient throughout the recovery period following the global financial crisis (GFC-2008) when growth was well under 3per cent for nearly a decade. Bangladesh’s share in world apparel exports is at 8per cent, but miniscule in case of non-RMG exports. Slower growth in OECD countries may only marginally impact RMG demand which should be compensated by redirection of orders away from China. Demand for our non-RMG exports (barely 16per cent of our export basket) should remain unaffected provided export diversification measures are actively implemented. What is more concerning is the persistence of inflation (albeit lower than in 2022) and prospects of interest rate hikes in major economies where the saying goes that interest rates are going to be “higher for longer”. In addition, if all the actions towards China decoupling and homeland economics protectionism come to roost this could result in inflation being “higher for longer”, that might not augur well for the world economy nor for developing economies like Bangladesh.

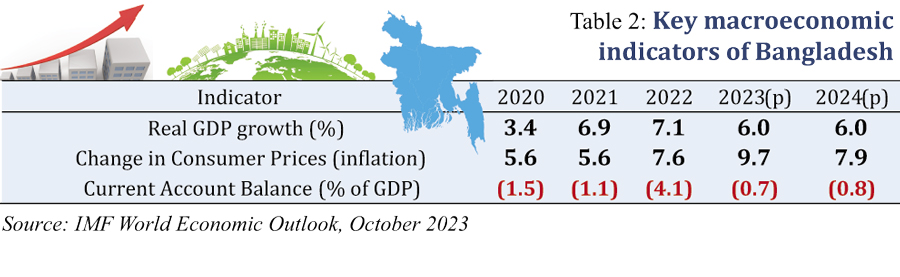

IMF’s latest WEO also makes assessment and projection of key macroeconomic indicators of the Bangladesh economy (Table 2), where growth projections appear significantly below official estimates but inflation and balance of payments data are consistent with official figures.

IMF’s latest WEO also makes assessment and projection of key macroeconomic indicators of the Bangladesh economy (Table 2), where growth projections appear significantly below official estimates but inflation and balance of payments data are consistent with official figures.

Only BBS has the capacity and paraphernalia for estimating national accounts and determining official figures of GDP and its growth rate. Nevertheless, leading multilateral agencies maintain the practice of making estimations and projections based on whatever high frequency macroeconomic and sectoral data is available in Bangladesh. Their estimates are still useful (with significant margin of error) as guidance about the state of the economy and its overall performance in the global context. BBS has recently announced that it has experimentally computed quarterly GDP estimates for the last five years, as one pf the commitments under the IMF credit program. Once finalized, this would fulfill a long-felt need for more credible annual GDP estimates.

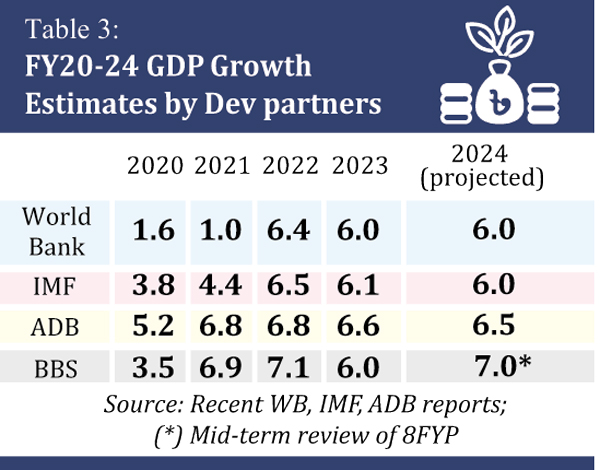

Given the backdrop of moderate growth in the global economy, leading multilateral agencies, WB, IMF, ADB, made growth projections for FY23 that are close approximations of the official estimate of 6.0per cent, though projections for FY24 diverges from the BBS official estimate (Table 3). ADB appears to be most optimistic during the current period (FY23-24) while official estimates for FY24 were revised downwards to 7.0per cent in the mid-term review of the 8th FYP in light of prevailing macroeconomic challenges, particularly the impact of import compression practiced by Bangladesh Bank to restore BOP stability and defend foreign exchange reserve position.

Given the backdrop of moderate growth in the global economy, leading multilateral agencies, WB, IMF, ADB, made growth projections for FY23 that are close approximations of the official estimate of 6.0per cent, though projections for FY24 diverges from the BBS official estimate (Table 3). ADB appears to be most optimistic during the current period (FY23-24) while official estimates for FY24 were revised downwards to 7.0per cent in the mid-term review of the 8th FYP in light of prevailing macroeconomic challenges, particularly the impact of import compression practiced by Bangladesh Bank to restore BOP stability and defend foreign exchange reserve position.

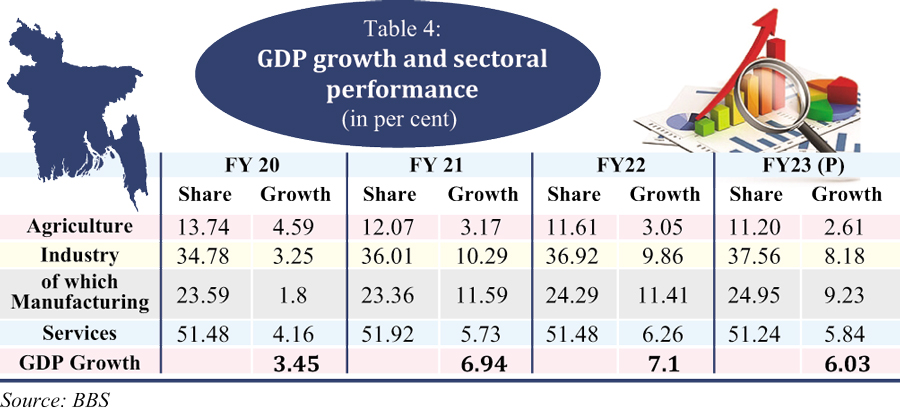

Bangladesh economy FY2023. Since the years of heady growth which spiked at 8.1per cent in FY2019, GDP growth has moderated since the downward shock of Covid in FY2020 when Bangladesh economy was among few economies that experienced positive but historically low growth of 3.5per cent (Table 4). After the strong post-Coved recovery produced GDP growth of 6.9-7.1per cent in FY21-22, in view of the aftermath of Russia-Ukraine war FY23-24 growth has been officially estimated at 6-7per cent, although development partners are less optimistic about 7per cent growth in FY2024, given the political climate and prevailing mismanagement of the macroeconomic and balance of payments challenges.

Manufacturing, export-oriented manufacturing in particular, is a key driver of rapid growth. Manufacturing growth rate, in the double digits for FY21-22, is expected to moderate in FY23 to 9.2per cent, resulting in lower but decent GDP growth of 6per cent, a rate that leading multilaterals also find acceptable in their

Manufacturing, export-oriented manufacturing in particular, is a key driver of rapid growth. Manufacturing growth rate, in the double digits for FY21-22, is expected to moderate in FY23 to 9.2per cent, resulting in lower but decent GDP growth of 6per cent, a rate that leading multilaterals also find acceptable in their  projections. We are waiting with bated breath to see the latest BB measures to become effective to rope in remittance through formal channels, exchange rate volatility tapering off, and official foreign exchange reserves stabilizing at comfortable levels, and domestic inflation moderating. Only then can we expect GDP growth rates of 7-8per cent to resume.

projections. We are waiting with bated breath to see the latest BB measures to become effective to rope in remittance through formal channels, exchange rate volatility tapering off, and official foreign exchange reserves stabilizing at comfortable levels, and domestic inflation moderating. Only then can we expect GDP growth rates of 7-8per cent to resume.

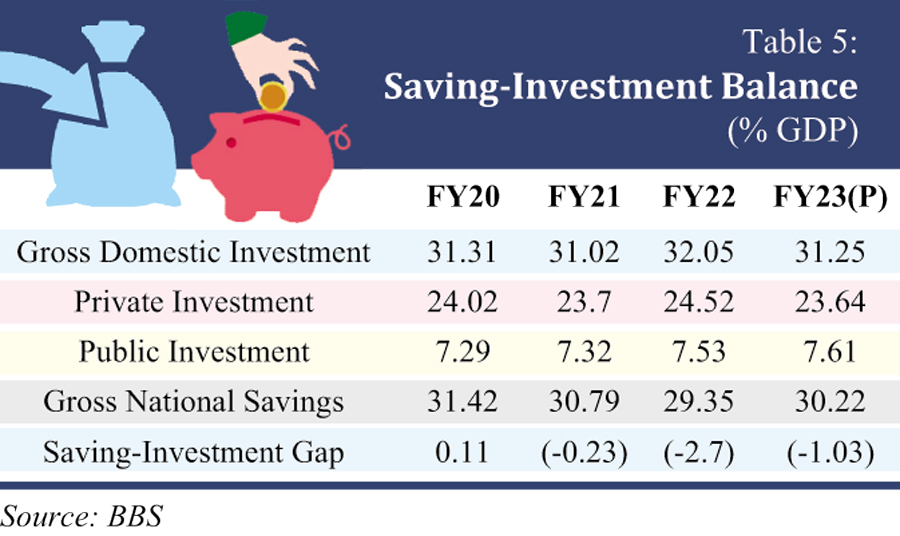

Growth in the  Bangladesh economy is still driven by investment, not consumption. Higher growth requires higher investment, both private and public. GDI has been hovering around 31per cent of GDP (Table 5) which is barely enough to generate GDP growth of about 7per cent, given an incremental capital-output ratio (ICOR) of around 4.5. So higher

Bangladesh economy is still driven by investment, not consumption. Higher growth requires higher investment, both private and public. GDI has been hovering around 31per cent of GDP (Table 5) which is barely enough to generate GDP growth of about 7per cent, given an incremental capital-output ratio (ICOR) of around 4.5. So higher  growth will require boosting investment rate to 35-36per cent on a sustained basis, which looks like a tall order now, given that private investment appears to be stalling for the past few years and higher investment would have to come from public investment that is also constrained by low domestic resource mobilization. The savings-investment gap continues to be modestly negative implying that the economy is investing more than its savings thus driving capital accumulation via foreign savings (mostly concessional loans).

growth will require boosting investment rate to 35-36per cent on a sustained basis, which looks like a tall order now, given that private investment appears to be stalling for the past few years and higher investment would have to come from public investment that is also constrained by low domestic resource mobilization. The savings-investment gap continues to be modestly negative implying that the economy is investing more than its savings thus driving capital accumulation via foreign savings (mostly concessional loans).

Bangladesh’s strong external balance under stress

For over 20 years Bangladesh has been accumulating foreign exchange reserves through modest surpluses in its overall BOP, thanks to robust double digit export performance and rising remittances, supplemented with moderate level of official development assistance (ODA, at 2-3per cent of GDP), which more than compensated for rising trade deficits in a growing economy. That comfort zone in external balances is now ruptured, first, on account of supply chain disruptions from the Russo-Ukraine war and, second, due to volatility in the exchange rate plus dwindling foreign exchange reserves, events partly due to ad hoc-ism and episodic handling of complex interlinked issues of domestic inflation, foreign exchange rate depreciation, and depletion of foreign exchange reserves. The general impression of analysts is for the crisis to intensify in the short run before it gets resolved in the medium- to long-term. Add to this the tense political climate, you now have the recipe for wide speculation about the direction of the economy in the near-term. One key indicator of the persistence of speculation is exchange rate volatility and the general sense that the central bank is falling short in its ability to tame the speculation geni which is out of the bottle.

A new expression, “dollar shortage”, has gained currency over the past year. In essence it implies that the demand for the greenback is well in excess of supply. Exports, remittances, and official development assistance (ODA) along with a modicum of FDI, generates the supply of dollars in the market as well as official FE reserves with Bangladesh Bank (BB). Demand for the greenback comes from imports of goods and services. As long as the perception of dollar shortage persists in the foreign exchange market, speculative behaviour will have the upper hand. The only way to dowse the fire of speculation is to create adequate supplies of dollars by roping in export and remittance inflows (plus as much ODA as possible).

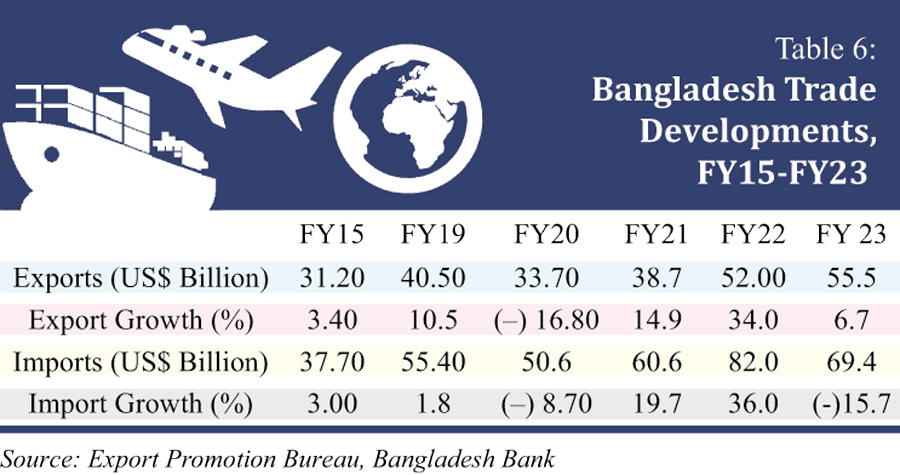

Severe import compression implemented by BB last year brought imports sharply down 15.7per cent (Table 6), thus resolving the gaping current account deficit (CAD) of FY22, but the move was neutralized by unprecedented deficit in the financial account of the BOP, something that did not occur in the past 25 years. Even IMF was surprised at this development as they had projected the usual surplus in the financial account based on past trend. In hindsight, IMF’s quantitative target of $24.5 billion Net Official Reserves appears quite unrealistic. BB focused on getting the CAD under control, which they did, but in the meanwhile the financial account moved from a surplus of $13 billion to a deficit of $2 billion, thus leaving an overall BOP deficit of $8 billion which depleted FE reserves further.

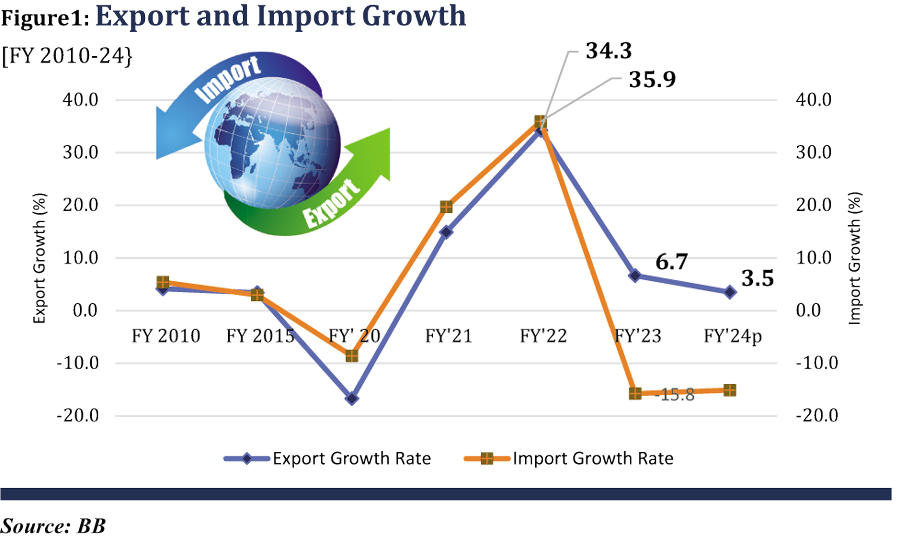

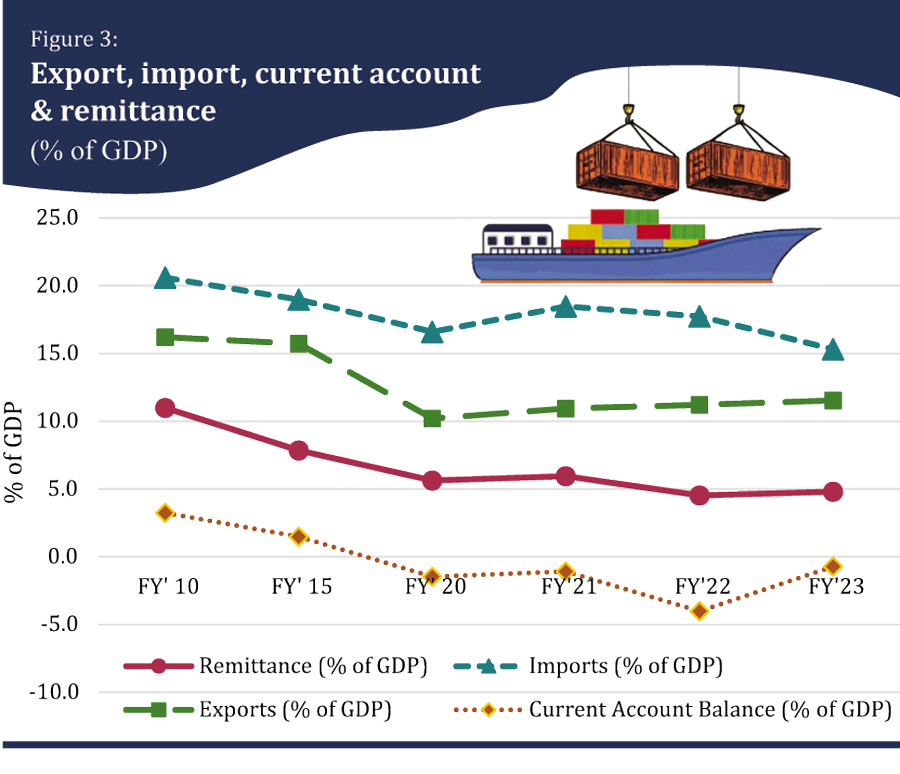

Export-import and remittance trends indicate that it is possible to restore stability in the BOP provided export receipts and inflow of remittances are effectively captured in BB’s FE reserves. In FY23, exports, remittances, ODA, brought in $88 billion ($7.5 billion/month), which should rise to about $95 billion in FY2024, even assuming a modest growth of exports (Fig.1). If imports (goods and services) could be held to $80 billion (a modest increase over FY23), the pressure on FE reserves as well as the exchange rate should ease, unless this trend is hobbled by unexpected rise in trade credit in the financial account. A caveat that needs to be added here is this scenario could be upset by unforeseen events related to the forthcoming elections and the persistent speculative behaviour in the FE market that could undermine inflows of remittance and even some export proceeds (potential capital flight).

Balance of Payments Management

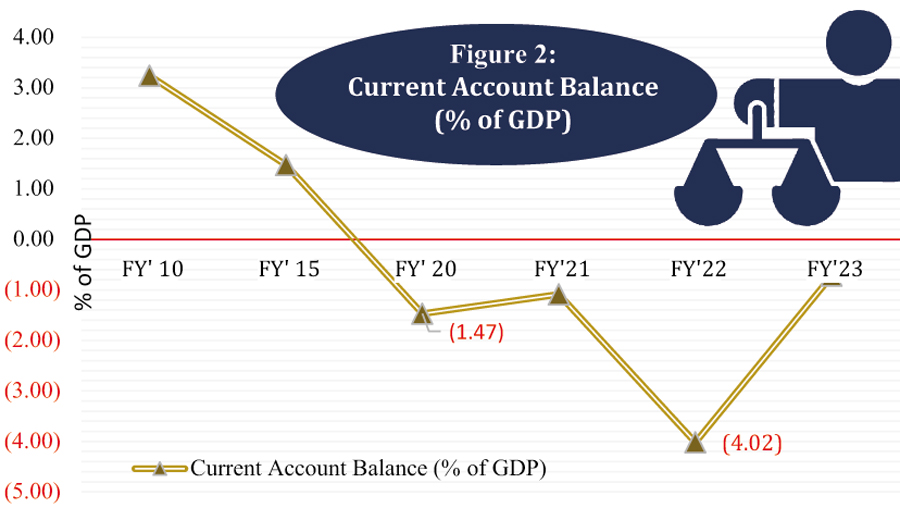

Deft macroeconomic management is warranted in the current state of BOP stress that emerged in the closing months of FY22 but continues as of this writing due to what may be construed as mismanagement. Thanks to Bangladesh Bank’s policy of import compression by strict administrative measures, the current account deficit returned to moderate levels (under 1per cent of GDP) and even turned positive in the first quarter of FY24 (Fig.2-3). Though this was a remarkable turnaround for a pivotal trade indicator, since it came about through severe import compression could have dire consequences for the productive sector of the economy including overall GDP growth. It is time to let the market determine import levels which will be constrained anyway due to the massive exchange rate depreciation which significantly raised import prices.

Deft macroeconomic management is warranted in the current state of BOP stress that emerged in the closing months of FY22 but continues as of this writing due to what may be construed as mismanagement. Thanks to Bangladesh Bank’s policy of import compression by strict administrative measures, the current account deficit returned to moderate levels (under 1per cent of GDP) and even turned positive in the first quarter of FY24 (Fig.2-3). Though this was a remarkable turnaround for a pivotal trade indicator, since it came about through severe import compression could have dire consequences for the productive sector of the economy including overall GDP growth. It is time to let the market determine import levels which will be constrained anyway due to the massive exchange rate depreciation which significantly raised import prices.

But the financial account continues to haunt the central bank. The financial account deteriorated substantially as import and exchange controls lowered foreign and domestic private investor confidence, which caused a drying up of private foreign credit, constrained the inflow of FDI and even contributed to capital flight. Overall balance, however, incurred a lower deficit during July-Sep of FY24 compared to that of FY23. The surplus in current account balance partially offset the deficit in financial account of USD 3.9 billion resulting in this lower deficit in overall balance during the period under review. If this trend could be maintained, end year FY24 BOP might return to its positive trajectory.

But the financial account continues to haunt the central bank. The financial account deteriorated substantially as import and exchange controls lowered foreign and domestic private investor confidence, which caused a drying up of private foreign credit, constrained the inflow of FDI and even contributed to capital flight. Overall balance, however, incurred a lower deficit during July-Sep of FY24 compared to that of FY23. The surplus in current account balance partially offset the deficit in financial account of USD 3.9 billion resulting in this lower deficit in overall balance during the period under review. If this trend could be maintained, end year FY24 BOP might return to its positive trajectory.

Foreign Exchange Reserves and Exchange Rate Management

The two are intricately related. Maintaining a level of FE reserves requires a policy of exchange rate flexibility. Thankfully, BB has realized the folly of running a scheme of multiple exchange rates that made matters worse but movement towards uniformity still remains incomplete. Instead of letting the exchange rate find its own level we observe ad hoc and episodic interventions continuing to the detriment of the FE reserve situation. You can’t have it both ways: i.e. maintain a FE reserve level and also keep the exchange rate fixed! Exchange rate flexibility is what prevents FE reserve level from depleting.

After futile attempts to hold on to an exchange rate of Tk.85 per US dollar, the Bangladesh Bank had to let go in April-May 2022 resulting in depreciation that has reached 30per cent (Tk.112/US$) without showing signs of settling down. The divergence between the kerb market rate and bank rates remains substantial (over 5-6per cent) and volatile, signifying instability in the foreign exchange market that prompts (a) inflows of remittance through unofficial channels (hundi), and (b) persistent speculation in the market about prospective rate hikes.

To shore up official FE reserves while preventing the exchange rate from moving to its market equilibrium rate seems to be an exercise in futility.

One thing to note, an exchange rate depreciation is inflationary. An exchange rate shock of the kind witnessed is even more inflationary when coupled with a spike in import prices. The price impact feeds through all traded and tradable goods in the domestic market and, eventually, fuels rise in price of non-traded goods (and services). The national inflation rate which was 6.2 per cent in March 2022 has approached 9.3 per cent as of Oct2023. A major part of this sharp rise in inflation can be attributed to the exchange rate shock.

By the end of June 2023, compared to June 2022, BB intervened and injected a total of 13.39 billion USD to prevent further depreciation of exchange rate. Notwithstanding BB’s effort to prevent the exchange rate from depreciating by injecting dollars from reserves, it has progressively depreciated with needless loss of reserves, that could have been protected by letting the exchange rate be market-determined and using demand management to stem the slide in the exchange rate. One more approach to compress imports by administrative controls is also turning into an exercise in futility. With 30per cent depreciation, imports are pricey enough to be contained by the market mechanism, not by administrative fiat (such as controlling LC opening).

The IMF program and FE Reserves

In the post–Covid19 world, IMF identified at least 53 most vulnerable economies, some of them on the verge of, if not already, approaching sovereign debt default. Ghana, Sri Lanka and Pakistan were in that group, not Bangladesh. Thanks to three decades of prudent macroeconomic management that ensured macroeconomic stability, IMF found Bangladesh to have low risk of debt distress with adequate capacity to repay the Fund which came up with a $4.7 billion support over a period of 42 months. IMF spokesman confirmed the support was not a rescue mission as in the case of Pakistan or Sri Lanka but meant to provide a buffer to achieve a comfort zone in Bangladesh’s FE reserves.

To be sure, the loans come with a reasonable agenda of reform efforts that have been mutually agreed between IMF and the Government (via an agreed Memorandum of Economic and Financial Policies (MEFP)). As economists we look at this as an opportunity for undertaking much needed structural reforms that would have positive long-term impacts to cope with the impending graduation from LDC status along with the nation’s goals for reaching Upper Middle Income Country (UMIC) status by 2031.

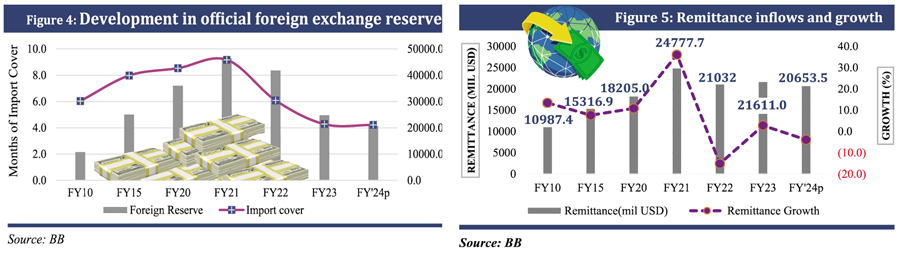

BB now computes the gross forex reserve following the BPM6 manual, excluding number of components including the export development fund (EDF) from computation. So, the gross FER (BPM6) stands at $20 billion as of Sep23 and net reserve is below $18 billion, which falls short of IMF’s program requirement of maintaining a net forex reserve of $24.4 billion. That places our reserve import cover at about four months if we use the IMF’s definition or five months if we use the government’s definition (Fig.4). Bangladesh Bank has to take corrective measures to regain lost reserves and letting the exchange rate adjust/float to market developments is the only viable option for them. Be that as it may, the second tranche release of about $650 million should in all likelihood come through shortly on the basis of justified ‘waivers’.

BB now computes the gross forex reserve following the BPM6 manual, excluding number of components including the export development fund (EDF) from computation. So, the gross FER (BPM6) stands at $20 billion as of Sep23 and net reserve is below $18 billion, which falls short of IMF’s program requirement of maintaining a net forex reserve of $24.4 billion. That places our reserve import cover at about four months if we use the IMF’s definition or five months if we use the government’s definition (Fig.4). Bangladesh Bank has to take corrective measures to regain lost reserves and letting the exchange rate adjust/float to market developments is the only viable option for them. Be that as it may, the second tranche release of about $650 million should in all likelihood come through shortly on the basis of justified ‘waivers’.

Using import compression by administrative means is not going to solve the problem but will impart damage to the productive sector of the economy. It is time to let the exchange rate float and compensate any inflation-triggering depreciation by reducing tariff rates (e.g. remove the 3per cent regulatory duty to start with, as an emergency measure) without any revenue loss (explained later).

In addition to exports of goods and services the other major source of foreign exchange and a key driver of the Bangladesh economy, including poverty reduction, is remittance from migrant workers. In essence, remittance is another form of exports – of factor services. Most migrant workers toil hard in foreign lands and send the bulk of their earnings home which in turn shores up official FE reserves, to the extent these come through formal channels. Hundi, the informal channel, remains alive at all times, and is particularly dominant when there is money to be made from the divergence between official and kerb market exchange rates, something that has been persisting with wide margins for the past 18 months or more. If current trends in the inflow of remittances continue, we can only hope to rope in remittances about the same as in FY23, about $22 billion (Fig.5). Sadly, with 1.4 million migrant workers leaving the country in FY23 (almost a 50per cent spike in migrant numbers), remittance inflows should have been at least $10-15 billion higher. We await with bated breath to see what innovative ways BB is resorting to in order to get more remittances into the official net. As long as the divergence between official and kerb market rates remain what it is, all the exercise we hear about will be futile.

Export Diversification stalls due to unfriendly Protection Regime

Before leaving the trade section of this report it is important to highlight the findings of a recent PRI research on export diversification challenge. One of the key drivers of the Bangladesh economy for the past decades has been the RMG industry. Taking advantage of the various facilities from the government including back-to-back letter of credit and duty-free bonded warehouse, the industry has turned out to become an export behemoth for the economy. Although the success of the RMG sector is commendable, being a one-track pony may not take Bangladesh very far and keep the engine of the economy running for too much longer. After graduating from the LDC status, Bangladesh will lose a large chunk of the preferential benefits that it now gets in the western markets, especially in the EU (albeit with a 3-year lag). That could potentially undermine dynamism in RMG exports for the future. That calls for renewed focus on building export-oriented industries for other types of products – a priority government agenda.

“Export diversification can lead to higher growth. Developing countries should diversify their exports since this can, for example, help them to overcome export instability or the negative impact of terms of trade in primary products.”

Nobel Laureate Economist Michael Spence, Chair of the Growth Commission.

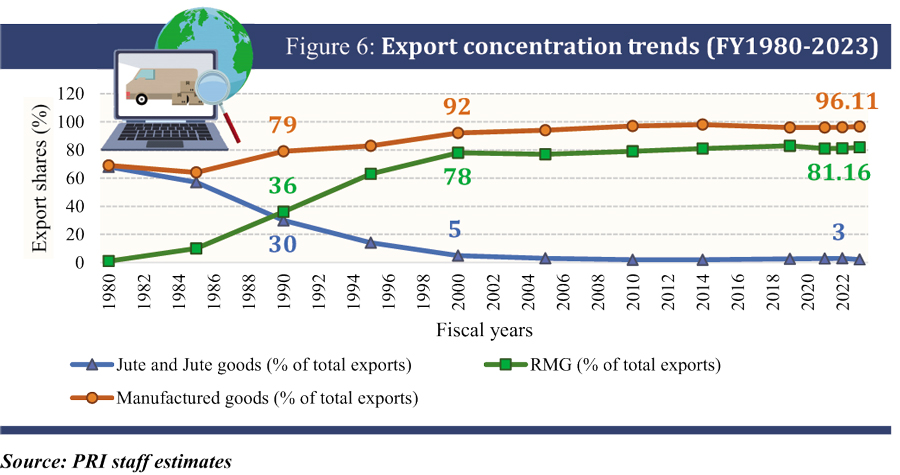

Fig. 6 captures the trend of export concentration in RMG over time. The share of RMG exports has risen from 30per cent in 1990, to 78per cent in 2000, and is now at 82-84per cent in 2022.  This trend towards concentration continues unabated. The share of RMG exports could hit 90per cent over the next five years, if this trend is not reversed by higher growth in non-RMG exports.

This trend towards concentration continues unabated. The share of RMG exports could hit 90per cent over the next five years, if this trend is not reversed by higher growth in non-RMG exports.

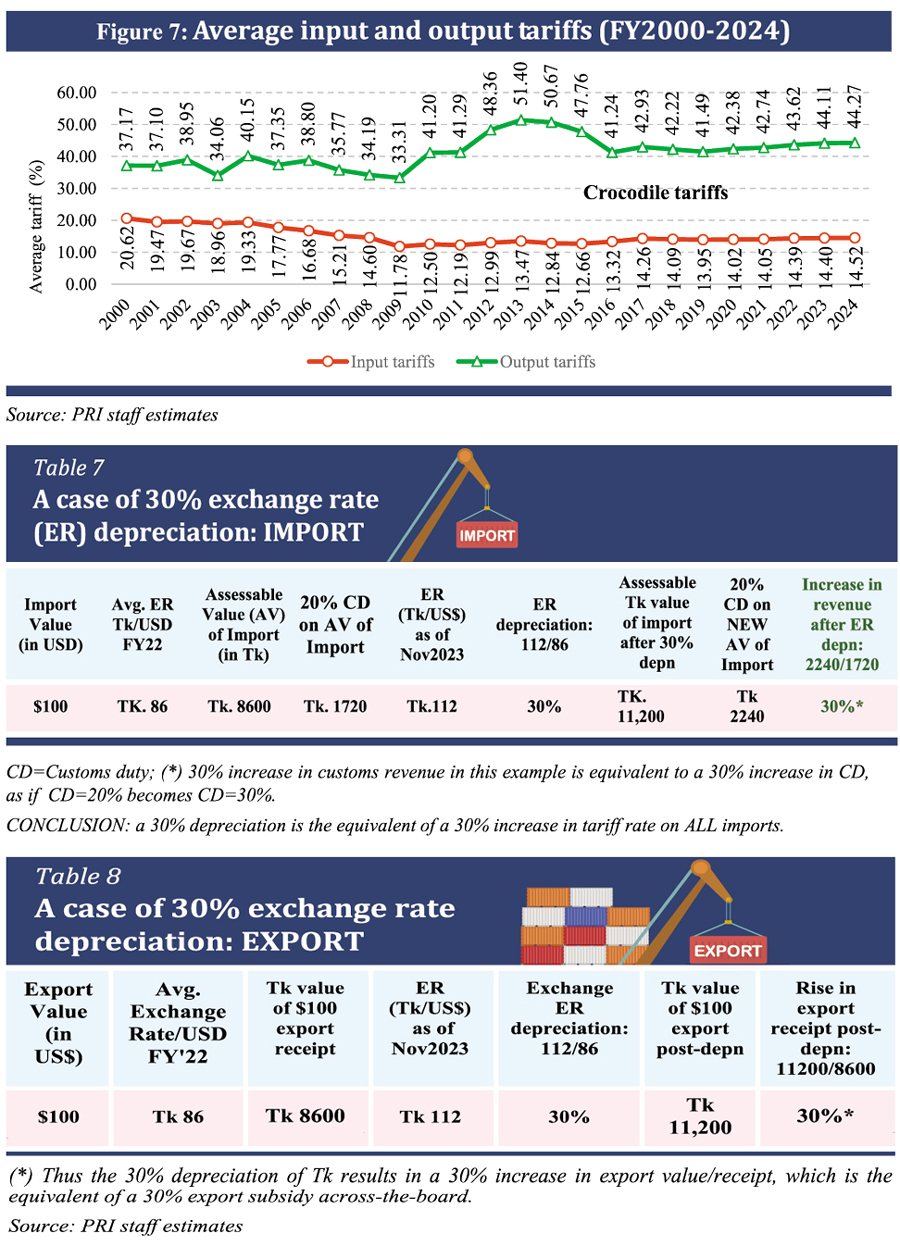

Bangladesh has a long and persistent history of protectionism in the tariff regime. As an LDC, Bangladesh has long stalled the rationalization of the tariff regime which is riddled with numerous WTO non-compliant para-tariffs. Apart from the initial wave of rationalization during the 90s, the tariff regime has been persistent on a protective stance since. Fig.7 shows how the average input tariffs have remained consistently lower than the average output tariffs, which in effect provides massive effective protection. This divergence in the average input and output tariffs give rise to Anti-export bias – the economic phenomenon where a country’s domestic economic policies and environment discourage exports in favor of sales in the domestic market. The principal source of this is the highly persistent tariff protection to import substitute industries. Tariffs on import substitute production are indirect subsidies that undermine exports. This subsequently makes domestic sales/import substitution more profitable. Recent PRI research has shown that the products of the RMG sector do not suffer from Anti-export bias, whereas the non-RMG products show evidence of high anti-export bias. This is because the RMG sector operates in a “free trade enclave” due to the Special Bonded Warehouse (SBW) system. Other exports do not operate under the same principle, thus giving rise to “trade policy dualism”. As long as domestic import substitution remains more profitable than exports in the case of non-RMG products, export diversification is unlikely to materialize. Therefore, the tariff regime acts as a binding constraint to export diversification.

With the launch of the new National Tariff Policy 2023, there is hope for a second wave of reforms in the tariff structure following WTO protocol. This new policy is going to introduce time-bound protection for identified high potential sectors rather than indiscriminate protection to the so-called infant industries. The idea of time-bound protection is appropriate with impending LDC graduation since the only way to ensure that our industries become competitive over time is by gradually reducing protective tariffs and increasing import competition thereby. The NTP 2023 is also introducing a scheme where all firms that produce for exports as well as sales in the domestic market will be able to import inputs (meant for exports) duty-free, by posting 100per cent bank guarantee against such imports, up to 70per cent of export value. As a result, this scheme will be the equivalent of Special Bonded Warehouse (SBW) granted to RMG exporters, something non-RMG exporters have been yearning for decades.

This policy is a step in the right direction since it will provide a level playing field for the non-RMG exports and help them gain market presence on a global scale. Besides the already established export-oriented RMG sector, if we can manage to find some other sectors focused exclusively on exports, our growth path following LDC graduation will be much smoother. Amid the impending reduction of preferential treatment in the western markets after LDC graduation, it is important for us to diversify beyond RMG as well as find new markets for our products.

Inflation must be tamed

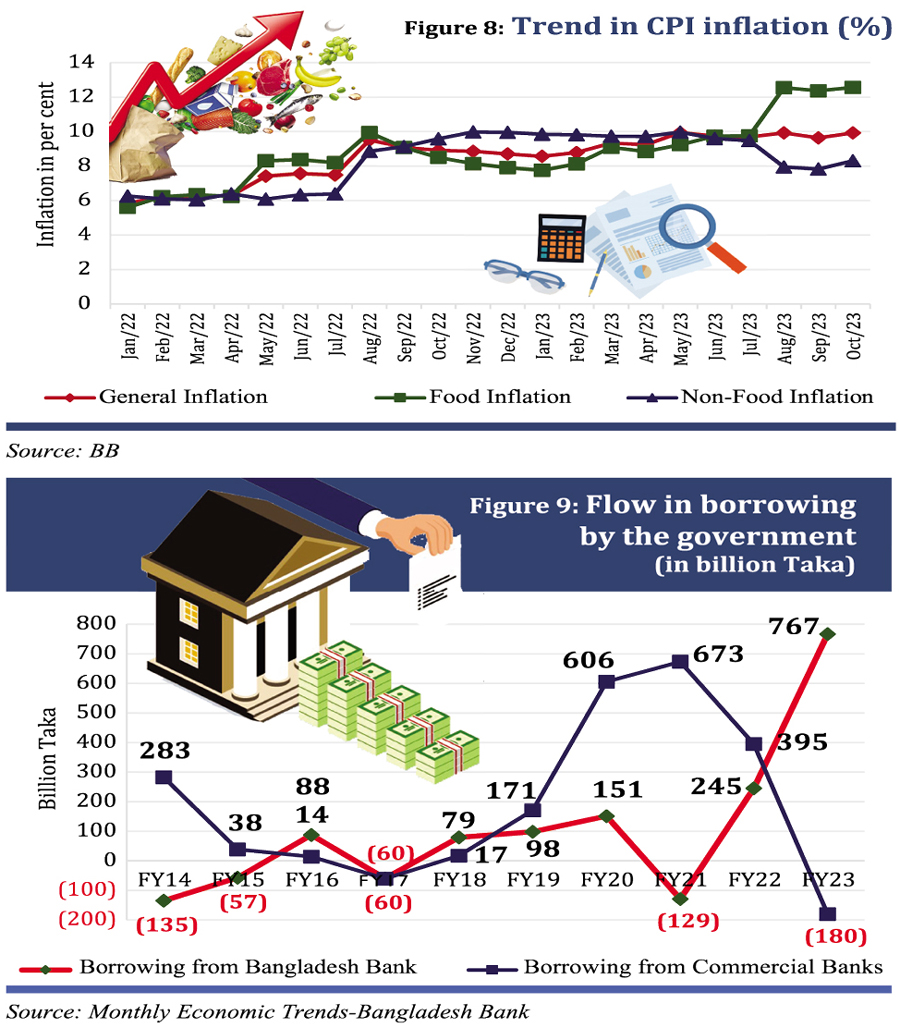

Inflation is now a problem to be reckoned with. The general rise in domestic prices was triggered by two simultaneous events in 2022: (a) the supply chain disruption of the Russo-Ukraine war that caused a spike in commodity prices, that is, the 3Fs: food, fuel and fertilizer; (b) the sharp depreciation of the Taka against the US dollar (nearly 30per cent as of Sep23). Though international commodity prices have abated somewhat, the second round effects of the two price triggers are having their impacts. Add to that the 50per cent hike in fuel prices by Government in August 2022. General inflation as of Oct23 is at 9.3per cent, with food inflation at over 12per cent (Fig.8). Suffice it to say that inflation, which is equivalent to a regressive tax, is hurting a wide swath of society, but its impact is more pronounced on the poor. It must be tamed, sooner rather than later.

Inflation is now a problem to be reckoned with. The general rise in domestic prices was triggered by two simultaneous events in 2022: (a) the supply chain disruption of the Russo-Ukraine war that caused a spike in commodity prices, that is, the 3Fs: food, fuel and fertilizer; (b) the sharp depreciation of the Taka against the US dollar (nearly 30per cent as of Sep23). Though international commodity prices have abated somewhat, the second round effects of the two price triggers are having their impacts. Add to that the 50per cent hike in fuel prices by Government in August 2022. General inflation as of Oct23 is at 9.3per cent, with food inflation at over 12per cent (Fig.8). Suffice it to say that inflation, which is equivalent to a regressive tax, is hurting a wide swath of society, but its impact is more pronounced on the poor. It must be tamed, sooner rather than later.

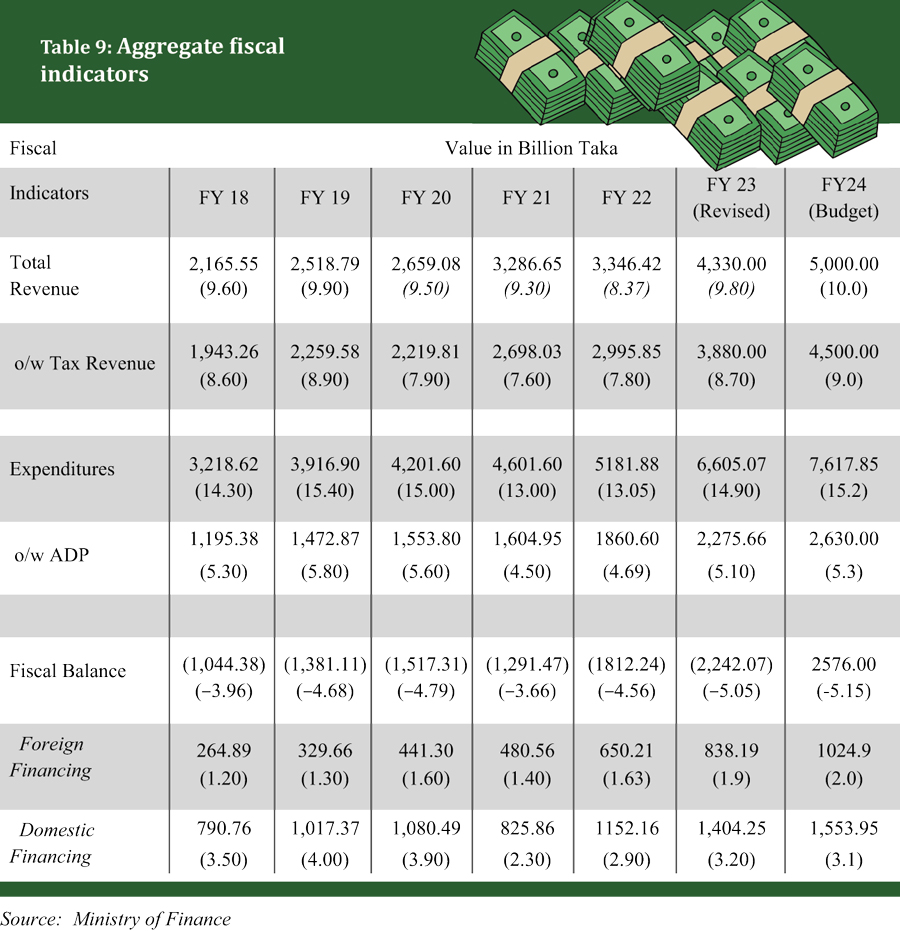

Long ago, the father of monetary economics, Milton Friedman, said that “inflation is always a monetary phenomenon”. That means, inflation is always associated with a rise in money supply. That view has been modified over time. Inflation can seldom be explained by demand-pull factors only, like rise in money supply, but includes cost-push factors like rise in input prices. Typically, inflation is the result of both demand and supply shocks, as is the case in Bangladesh. The impact of supply chain disruption and exchange rate depreciation was a supply shock that triggered inflation which was reinforced by monetary expansion. The latter has now been reversed by BB through the standard prescription of monetary contraction and interest rate hikes (modest). Also, the tendency to finance the budget deficit through borrowing from BB (which is pure inflationary money creation) has also been suspended (Fig.9) as of July23.

In the Bangladesh context, the preceding standard prescription may only restrict demand but does not do anything to counter the supply shock emanating from import price hike plus depreciation. Indeed, the severe import compression imposed on the economy by BB is likely to raise import costs (scarcity driven) thus becoming a cost-push factor of inflation. This is where our current tariff structure presents a uniquely Bangladeshi opportunity to counter the inflationary effect of depreciation through an approach that can be described as “compensated depreciation”.

An illustration follows. Since May 2022, Bangladesh Taka has depreciated more than 30per cent against the US dollar.

The substantial inflation-trigger prompted by the massive depreciation sustains inflation as no compensating countermeasures are in sight nor even talked about. What goes unnoticed is its effect on exports, imports, and inflation. Below (Table 7-8) is a simple illustration of the depreciation impact on export receipts, import tariffs, and domestic inflation.

1. The 30per cent depreciation that occurred over FY22-23 has resulted in a 30per cent subsidy on ALL exports and a 30per cent increase in Tariff rate on ALL imports.

2. The subsidy effect on exports will give a boost to all exports. However, the higher cost of imported inputs will somewhat moderate the subsidy impact, primarily on non-RMG exports.

3. This subsidy also applies to all remittances which should get a tremendous boost. Yet HUNDI remains widely prevalent due to the divergence between bank and kerb market rates.

4. The higher tariff impact on ALL imports is real. It has raised the price of ALL imports by roughly the amount of the depreciation with consequential impact on customs revenue. However, the total impact on NBR customs revenue from the upward price effect will depend on how much import demand will be reduced on account of higher import price. Nevertheless, it creates the unprecedented scope for tariff remission without revenue loss.

5. The upward import price effect of the depreciation will obviously raise the cost of imported inputs and affect profitability of production for the domestic market.

6. The rise in import price due to depreciation has fueled domestic inflation which is stubbornly holding at around 9-10per cent.

A downward shock to inflation could be brought about by a downward tariff adjustment – described as “compensated depreciation”. Any downward tariff adjustment would partly neutralize the price or inflationary impact of depreciation – swiftly and sharply. This would be a radically and uniquely Bangladeshi approach to counter inflationary impact of depreciation, if the objective is to tame inflation swiftly and sharply. The argument that tariff cut will cause loss of revenue is not valid in this case as ALL tariffs have increased 30per cent across-the-board due to depreciation. Furthermore, using exchange rate depreciation as a strategy for revenue mobilization cannot be a valid tax effort. Tariff remission of 5-10-15per cent (from existing rates) will have immediate effect on domestic prices of imports as well as import substitutes and costs of production. This is one great opportunity to remove Regulatory Duty (RD), as an emergency measure to control inflation. More can and should be done in the next Budget FY25.

Inflation and Food security

The role of agriculture cannot be underestimated, though its share in GDP has been falling. Its contribution to our food security is critical.

Bangladesh began its journey in 1971 as a food deficit country with 70 million mouths to feed, with 10 MMT of rice production which was 10per cent short of domestic requirement. The deficit was met with food aid and imports. Food aid is now history having disappeared from the radar in the 1990s.

In the past five decades, both rice output and productivity (MT/ha) quadrupled. Rice (the staple food) production has quadrupled to over 40 MMT in 2023 while the population rose 2.5 times to 170 million, making the country nearly self-sufficient in food.

Since 2001, the government has proactively maintained the per capita availability of rice above the required levels, ensuring an adequate quantity in storage to address emergencies. As a result, per capita availability has consistently exceeded requirements indicating robust food security, in terms of availability.

Nevertheless, access to food (i.e., the second dimension of food security) may be impeded by the emergence of ‘entitlement failure,’ a concept defined by Nobel laureate Amartya Sen. Entitlement failure can occur despite an adequate supply of food due to lack of purchasing power of marginalized groups. If current rate of inflation persists, it could cause slippage of large numbers into poverty thus creating conditions of entitlement failure. Taming inflation swiftly has therefore become a national imperative.

Other dimensions, such as optimal food utilization (i.e., minimizing post-harvest losses and reducing food waste, efficient and effective food processing techniques) and reliable food stability (such as maintaining stockpiles to address short-term disruptions like natural disasters or emergencies), also contribute to overall food security.

Fiscal restraints and revenue mobilisation challenge

Macroeconomic stability alongside fiscal prudence has long been the hallmark of Bangladesh’s fiscal policy in the sense that despite weak revenue mobilisation effort, public expenditures have stayed within the resource constraints to deliver budget deficits averaging 3.9per cent of GDP until FY2019 – a highly sustainable fiscal indicator. That situation changed only modestly rising to 5.1 per cent in FY2023 (Table 9). Inflation and BOP stress have recently put internal and external macroeconomic stability on the dock. Restoration of macroeconomic stability is partially tied to the formidable challenge of enhancing revenue mobilization. Historically, our revenue mobilization effort has not kept pace with economic expansion. It was always a policy debate on how we could increase our resource mobilization and improve the tax-GDP ratio. The recent IMF loan programme has also emphasized domestic revenue mobilization putting key quantitative requirements for increases in revenue mobilization efforts with additional 0.5per cent of GDP annually in FY24 and FY25 and 0.7per cent of GDP in FY26.

Macroeconomic stability alongside fiscal prudence has long been the hallmark of Bangladesh’s fiscal policy in the sense that despite weak revenue mobilisation effort, public expenditures have stayed within the resource constraints to deliver budget deficits averaging 3.9per cent of GDP until FY2019 – a highly sustainable fiscal indicator. That situation changed only modestly rising to 5.1 per cent in FY2023 (Table 9). Inflation and BOP stress have recently put internal and external macroeconomic stability on the dock. Restoration of macroeconomic stability is partially tied to the formidable challenge of enhancing revenue mobilization. Historically, our revenue mobilization effort has not kept pace with economic expansion. It was always a policy debate on how we could increase our resource mobilization and improve the tax-GDP ratio. The recent IMF loan programme has also emphasized domestic revenue mobilization putting key quantitative requirements for increases in revenue mobilization efforts with additional 0.5per cent of GDP annually in FY24 and FY25 and 0.7per cent of GDP in FY26.

Fiscal deficits are a part and parcel of any developing economy. Thankfully, Bangladesh has been investing fiscal resources generated through these deficits as shown by the striking equality of ADP with fiscal deficits, year after year. Therefore, understanding and managing sustainable fiscal policies involves paying close attention to two key factors: the size of the fiscal deficit and how it’s being funded. The least cost option is foreign financing (typically kept at 40per cent of the deficit, with 60per cent coming from domestic sources). As for size, deficits of under 5per cent of GDP are recognized as sustainable. A particular concern is the potential inflationary impact and the risk of crowding out private economic activities resulting from fiscal deficits. When funded through increased bank borrowing, the impact is inflationary (more so if financed through borrowing from BB), while financing through private sources (e.g. shanchaypatra) may constrict the accessibility of bank credit causing crowding out of private investment. To avoid these negative impacts – inflation and lower investment – it is imperative to enhance tax effort and raise the tax-GDP ratio, as IMF program entails.

Recently, the tax earnings from both import-based and domestic-based taxes have consistently increased in absolute amounts due to the higher exchange rate, and inflation. The latest trends also indicate the prospect of higher revenue mobilization in the current fiscal year. The National Board of Revenue (NBR) demonstrated an impressive performance in revenue collection, the government fell short of the IMF target by a margin of only BDT 66 billion (2per cent shortfall). The absolute earnings from both non-NBR and non-tax revenue are expected to grow compared to the last fiscal year, assuming there is return to normalcy post-election.

Recent tax revenue data (as of Sep23) shows promise of higher revenue mobilization in FY24, particularly from customs. As mentioned earlier, NBR revenue has received a boost from the massive depreciation of over 30per cent since May 2022. This is tantamount to a 30per cent hike in ALL tariffs. However, import compression measures by BB have substantially reduced imports (15per cent in FY23), the net result is still positive. In the first quarter of FY24, NBR collected BDT 767.5 billion tax revenue, while the IMF’s tax revenue target required BDT 615.6 billion. The recent revenue performance of the NBR instills optimism that the government can attain the IMF revenue target for FY24 through strategic corrective interventions. In this context, it is imperative to implement time-bound policy measures to address persistent revenue challenges, ensuring long-term fiscal sustainability and fostering accelerated economic growth.

Prudent Debt Management thus far

Deficits create public debt obligations. The government has so far managed the budget deficit in a sustainable manner below 5per cent of GDP, despite the challenge of a low tax-GDP ratio. Consequently, public debt obligations have remained sustainable. It is a good sign that the government regularly increased the budget size without increasing the deficit-GDP ratio. In recent times, various factors have contributed to the modest augmentation of the budget deficit, including the initiation of multiple development and mega projects and the implementation of an expansionary budget to mitigate the aftermath of the Covid-19 pandemic. While these measures have resulted in an increased budget deficit, they have concurrently played a pivotal role in the economic recovery process, fostering overall economic growth.

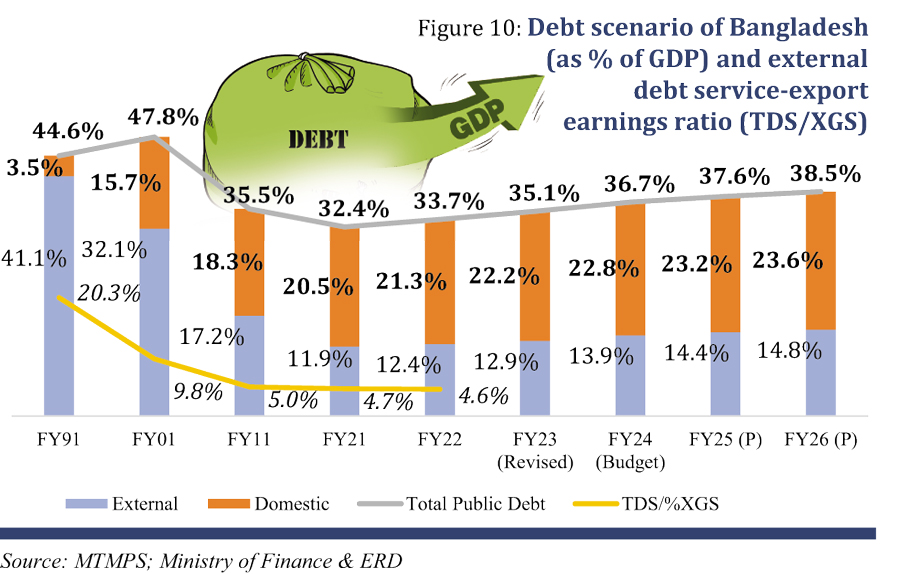

The government usually borrows from domestic and external sources to finance this budget deficit. Till now, Bangladesh has successfully maintained the public debt-GDP ratio on average around 32per cent in the last decade, while it was more than 44per cent in the early 90s. However, it is estimated to go up to 38.5per cent by FY26, which is still below debt sustainability threshold of 55per cent (Fig.10).

Moreover, there is an observed trend where the proportion of debt sourced domestically (as per cent of GDP) is expanding faster than the diminishing trajectory of external sources. This has dual implications: firstly, the government’s reduced dependence on external sources, and secondly, the potential crowding out effect on domestic sources, constricting lending alternatives for the private sector. However, the total public sector external debt service to FE earnings ratio has diminished, portraying a better situation at mere 4.6per cent. Moreover, the public sector external debt approached $75 billion, while private sector external debt decreased by $4 billion in FY23 from $26 billion in FY22

Moreover, there is an observed trend where the proportion of debt sourced domestically (as per cent of GDP) is expanding faster than the diminishing trajectory of external sources. This has dual implications: firstly, the government’s reduced dependence on external sources, and secondly, the potential crowding out effect on domestic sources, constricting lending alternatives for the private sector. However, the total public sector external debt service to FE earnings ratio has diminished, portraying a better situation at mere 4.6per cent. Moreover, the public sector external debt approached $75 billion, while private sector external debt decreased by $4 billion in FY23 from $26 billion in FY22

The recent depreciation of BDT put pressure on the debt services and repayment. A Finance Division assessment reveals that a 10per cent depreciation in BDT/USD exchange rates will elevate public debt by BDT 50 billion, reaching Tk. 402 billion by the end of FY24. Additionally, this depreciation amplifies Taka project costs, primarily funded through external borrowing.

However, comparing public and private external debt involves contrasting entities. Most short-term private external debt comes from trade credit, primarily advance payments for export orders, minimally impacting the BOP. No strict rules govern a country’s external debt limits. IMF and World Bank suggestions are not rigid guidelines, allowing countries to establish their own rules, considering these recommendations as a starting point. It all depends on an economy’s growth rate. If the economy is growing fast, taking on more external debt might be okay.

Epilogue…..navigating through global and domestic firestorms

As the sun sets on the year 2023, firestorms are raging in the domestic as well as the world markets. This calls for the most competent and rigorous diagnosis of the challenges facing the economy and crafting appropriate, even innovative and distinctly Bangladeshi, policies to cope with the situation. The immediate challenge is to restore macroeconomic stability – internal and external – in order to restore the economy’s long run growth trajectory. Before the troika of inflation, FE reserve depletion, and exchange rate volatility turn into a hydra-headed monster. In this regard, as evidence has shown, half-hearted and episodic measures will prove futile. Post-elections, a new and definitive round of holistic economic reforms are long overdue.

Domestically, tax reforms need to be given the highest priority post-elections. The current tax regime is neither pro-business nor revenue enhancing and has proved to be a stumbling block to the dynamism and competitiveness of the economy. There is conclusive research evidence that Bangladesh’s topmost challenge and policy priority – export diversification – is facing a binding constraint from high protective tariffs that instill deep-rooted anti-export bias of incentives. The launch of a National Tariff Policy 2023 is a major step in the right direction whose implementation holds the promise of unleashing the forces of export diversification.

In international trade, a 75-year Bretton Woods era that recognized international trade as a transformative force for global prosperity is perhaps coming to a close. Trade interventions are on the rise, in the form of production subsidies, import restrictions based on national security, export controls to punish geopolitical rivals, and so on. But what is replacing the old economic order does not appear palatable for developing economies like Bangladesh that effectively leveraged the world market for developing an export-oriented manufacturing base creating jobs for the vast reserves of its unemployed labor force, especially women. Rising homeland economics, re-shoring or friend-shoring are but protectionism in different garbs. More bothersome is the tendency for meshing national security (called strategic autonomy) with economic policy. Globalization that produced efficiency dividends like global value chains (GVCs) might appear to be on the back foot, but, thankfully, recent studies by leading trade economists still confirm that there is no conclusive evidence that international trade is deglobalizing (or declining); only that the era of “hyperglobalization” is effectively over. In this evolving global landscape, Bangladesh economy has ample potential to thrive.

Then there is China+1 geopolynomics, a de-risking alternative to unbridled GVCs that seeks to limit China’s rise as an economic or technocratic superpower. As the world’s No.2 exporter of apparels after China, this opens opportunities for Bangladesh to seize as some $100 billion of apparel orders are expected to shift out of China in the next few years and our RMG industry is well placed to absorb part of this additional demand given its wage competitiveness, under-utilized production capacities, and capable swift-footed first-generation entrepreneurs.

To conclude, what is evolving globally is not the end of globalization, a phenomenon that has its own inexorable momentum. It is good that globalization will be changing to become aligned with 21st century world trade in goods and services. Regardless, Bangladesh’s latent potential for economic prosperity will be best harnessed by leveraging the world market via international trade for many years to come.

Dr. Zaidi Sattar is Chairman, Policy Research Institute of Bangladesh (PRI). zaidisattar@gmail.com

Members of the PRI Research Team who provided research support to this report:

Dr. Masudul Haque Prodhan, Economist, Promito Musharraf Bhuiyan, Senior Research Associate, Sumaiya Fatima Farah, Senior Research Associate, Karisa Musrat, Senior Research Associate, Tasdid Mohammed Fayed, Senior Research Associate, Md. Salay Mostofa, Senior Research Associate, Md. Salay Mostofa, Senior Research Associate